把握美國財報季交易機會

2026年第一季財報季或將迅速引發市場波動。事先關注重點財報時間,規劃您的觀察清單,借助專為活躍交易者打造的工具,靈活交易美股 CFDs。

Most watched this season

Apple • Microsoft • Alphabet • Amazon • Nvidia • Meta • Tesla

與 GO Markets 一起交易美國財報季

美國財報季期間,眾多大型上市公司將陸續公佈業績。財報結果、業績指引及市場預期的變化,往往會在短時間內對個股、行業板塊甚至整體指數造成顯著影響,市場波動隨之加劇。

具競爭力的交易成本

在財報公布等行情快速變化時段,幫助您更好管理交易成本。

專業技術分析工具

利用圖表與技術指標,輔助您制定入場、出場及風險管理策略。

為活躍交易者打造

穩定可靠的交易平台,搭配快速執行,滿足高頻與短線交易需求。

風險管理功能

使用內建風控工具,在波動行情中更清楚控制下行風險,保護持倉。

更多交易時間

部分美股 CFDs 支援延長交易時段,讓您在常規市場時間之外亦可把握交易機會。*

*不同產品的可交易時段有所差異,非正常交易時段的交易條件可能不同。

本財報季重點關注

美國財報日曆

顯示的時間採用澳洲東部標準時間(GMT+10)。您可隨時在「收益日曆」設定中變更時區。

市場資訊與分析

Expected earnings date: Wednesday, 28 January 2026 (US, after market close) / early Thursday, 29 January 2026 (AEDT)

Key areas in focus

Intelligent Cloud (Azure)

Azure remains Microsoft’s primary earnings swing factor. Markets are watching to see whether any growth reflects demand strength or capacity constraints, and how AI-related workloads are impacting margins.

Productivity and Business Processes

Microsoft 365, Office, and LinkedIn are sources of recurring revenue for Microsoft. Growth, pricing discipline, and client churn remain the key variables that markets will be watching.

Personal Computing

Windows, devices, and gaming are more cyclical. Stabilisation of PC demand and gaming engagement remain secondary sources of revenue but are still noteworthy.

Artificial intelligence

Approaches around the monetisation of Microsoft’s AI play are still developing. Trends in enrolment and infrastructure cost are expected to be key factors.

What happened last quarter

Microsoft reported results ahead of consensus, supported by steady cloud demand and resilient enterprise software revenues.

Azure and other cloud services' growth remained a central focus, alongside commentary on AI-related investment and capacity.

Last earnings key highlights:

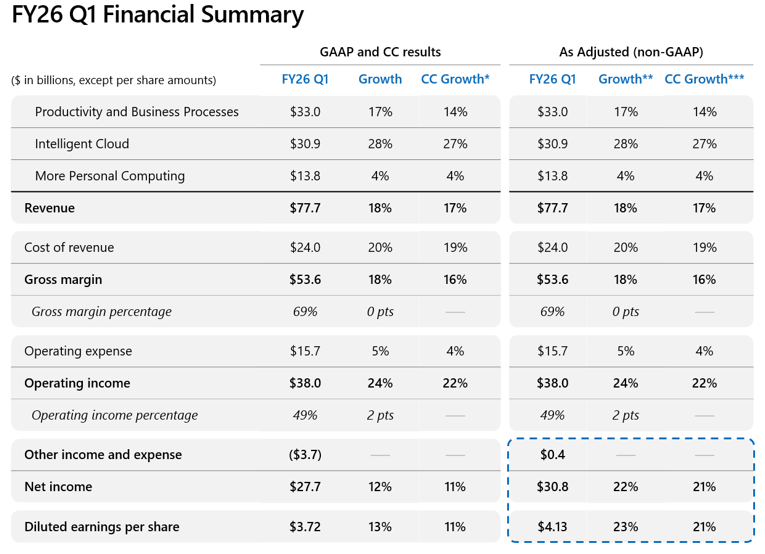

- Revenue: US$77.7 billion

- Earnings per share (EPS): US$3.72 (GAAP) and US$4.13 (non-GAAP adjusted)

- Intelligent Cloud revenue: US$30.9 billion

- Azure and other cloud services: up 40% year on year

- Operating income: US$38.0 billion

How the market reacted last time

Microsoft shares fell in after-hours trading following the release, despite the beating of headline numbers, as investors focused on AI investment intensity, capacity constraints and related implications for future margins.

What’s expected this quarter

Bloomberg consensus points to continued revenue growth led by cloud services, alongside broadly stable margins despite elevated capex.

Bloomberg consensus reference points (January 2026):

- Revenue: about US$68 to US$69 billion

- EPS: about US$3.10 to US$3.20 (adjusted)

- Azure growth: mid-to-high 20% year on year (YoY) (constant currency)

- Operating margin: expected to remain broadly stable

- Capex: expected to remain elevated, reflecting AI and cloud build-out

*All above points observed as of 16 January 2026.

Expectations

Sentiment appears cautious. Microsoft can remain sensitive to any cloud, margin, or guidance disappointment, particularly where investors interpret investment intensity as open-ended.

Price action traded within an established range of US$472 and US$490 recently, but has moved below this in the last week.

Listed options were pricing an indicative move of around ±2% based on near-dated options expiring after 28 January and an at-the-money options-implied ‘expected move’ estimate.

Implied volatility was about 33.5% annualised into the event as observed on Barchart at 11:00 AEDT on 16th January 2026.

These are market-implied estimates and may change; actual post-earnings moves can be larger or smaller.

What this means for Australian traders

Microsoft’s earnings may influence near-term sentiment across US technology indices, particularly the Nasdaq, with potential spillover into global equity risk appetite and, in turn, the ASX.

As a major technology stock, and with Tesla (TSLA) also scheduled to report after the US close on the same day, volatility in Nasdaq-linked products may increase while futures markets remain open.

Important risk note

Immediately after the US close and into the early Asia session, Nasdaq 100 (NDX) futures and related CFD pricing can reflect thinner liquidity, wider spreads, and sharper repricing around new information.

Such an environment can increase gap risk and execution uncertainty relative to regular-hours conditions.

Expected earnings date: Wednesday, 28 January 2026 (US, after market close) / early Thursday, 29 January 2026 (AEDT)

Key areas in focus

Advertising (Family of Apps)

Advertising remains Meta’s dominant revenue driver. AI-driven ad targeting, Reels monetisation, and engagement efficiency can be important contributors to revenue growth and may support advertiser outcomes, noting results can vary by advertiser, format, and market conditions.

User engagement and monetisation

Engagement trends across Facebook, Instagram, WhatsApp, and Threads remain closely watched as indicators that can influence monetisation assumptions and medium-term expectations.

Artificial intelligence

Meta views AI as a foundation for content discovery, advertising performance, and the development of generative tools. Markets may continue to evaluate whether AI-driven gains offset the level of infrastructure and data centre investment required to support these projects.

Reality Labs

Reality Labs remains loss-making. Management continues to frame AR/VR and metaverse-related platforms as long-term strategic investments, while acknowledging continued operating losses and a drag on earnings performance.

What happened last quarter

Meta’s most recent quarterly update highlighted strong revenue growth alongside ongoing investment themes.

The company’s reported (GAAP) net income and EPS reflected a one-time, non-cash income tax charge disclosed in the earnings materials, while management commentary also emphasised cost discipline and investment priorities.

Operating margins expanded year-on-year, despite elevated AI-related investment.

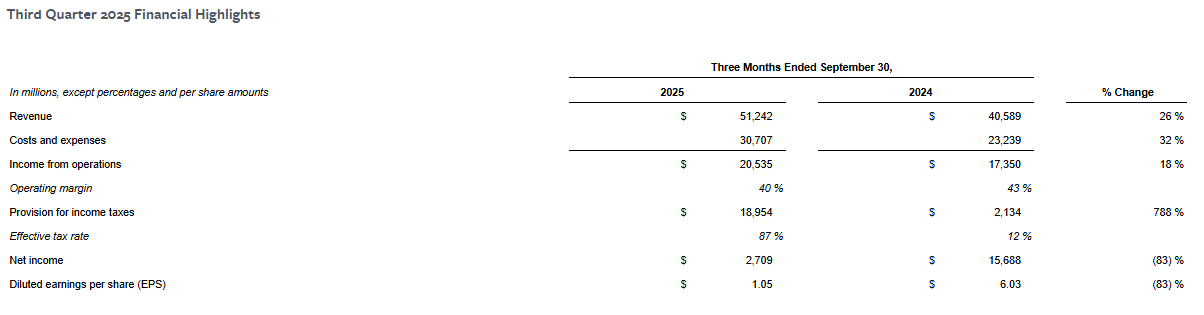

Last earnings key highlights

- Revenue: US$51.24 billion

- Earnings per share (EPS): US$1.05 (GAAP)

- Advertising revenue: US$50.08 billion

- Operating margin: 40%

- Reality Labs operating loss: about US$4.43 billion

How the market reacted last time

Meta shares fell in after-hours trading after the release. Commentary at the time highlighted strong top-line outcomes, alongside investor focus on the outlook for spending and the pace of AI and infrastructure investment.

What’s expected this quarter

Bloomberg consensus points to continued year-on-year revenue growth, led by advertising, with operating margins expected to remain elevated despite ongoing AI and infrastructure expenditure.

Bloomberg consensus reference points (January 2026)

- Revenue: about US$41 to US$43 billion

- EPS: about US$4.80 to US$5.10 (adjusted)

- Advertising growth: high-teens year on year (YoY)

- Operating margin: expected to remain above 40%

- Capital expenditure (capex): elevated, reflecting AI and data centre investment

*All above points observed as of 23 January 2026.

Expectations

Sentiment around Meta Platforms may be sensitive to any disappointment around advertising demand, margin sustainability, or the scale of ongoing investment in AI and Reality Labs.

Recent price action suggests that some market participants appear to be pricing in a relatively constructive earnings outcome, which can increase sensitivity to negative surprises.

Listed options were pricing an indicative move of around ±3% based on near-dated options expiring after 28 January and an at-the-money options-implied ‘expected move’ estimate.

Implied volatility was about 31% annualised into the event, as observed on Barchart at 11:00 am AEDT on 23 January 2026.

These are market-implied estimates and may change. Actual post-earnings moves can be larger or smaller.

What this means for Australian traders

Meta’s earnings may influence near-term sentiment across US technology indices, particularly the Nasdaq, with potential spillover into broader global equity risk appetite and index-linked products traded during the Asia session after the release, which can be volatile and unpredictable following earnings events.

Important risk note

Immediately after the US close and into the early Asia session, Nasdaq 100 (NDX) futures and related CFD pricing can reflect thinner liquidity, wider spreads, and sharper repricing around new information.

Such an environment can increase gap risk and execution uncertainty relative to regular-hours conditions.

Australian CPI may test market pricing for a February RBA move, while the Federal Reserve narrative will be followed closely, even though a pause is widely expected. It is also a busy US earnings week, with mega-cap names headlining, and Gold remains a key market focus.

- Australia CPI: Australian CPI is the key domestic release, with markets pricing the risk of a February RBA rate increase.

- US Federal Reserve: The Fed is widely expected to hold rates steady, with attention on whether a potential June rate cut remains intact.

- US mega-cap tech earnings: Earnings from large-cap technology names may test whether current equity valuations remain supported.

- Gold: Gold continues to trade near record highs.

Australia

- Australia CPI (Q4): Wednesday, 28 January

Stronger-than-expected jobs report this week lifted market expectations for further policy tightening.

According to the ASX RBA Rate Tracker, market-implied pricing for a February rate increase has risen to above 60%.

Market impact

- AUD crosses may respond to any shift in rate expectations

- Rate-sensitive equity sectors could see follow-through moves

Federal Reserve

- FOMC rate decision: Wednesday, 28 January (US) | 29 January (AEDT)

The Federal Reserve is widely expected to announce no change in rates after its two-day meeting.

Market focus will centre on communication around inflation progress, and whether market-implied pricing for a potential June rate cut is reinforced or challenged.

Market impact

- USD direction may respond to any shift in policy tone across multiple asset classes

- US Treasury yields, especially at the front end, may react to changes in rate expectations

US mega-cap earnings

- Boeing: 27 January (US time) | 28 January AEDT

- Microsoft: 28 January (US time, after market close) | 29 January AEDT

- Meta Platforms: 28 January (US time, after market close) | 29 January AEDT

- Tesla: 28 January (US time, after market close) | 29 January AEDT

- Caterpillar: 29 January (US time, before market open)/30 January AEDT

- Apple: 29 January (US time, after market close) | 30 January AEDT

Earnings from US mega-cap technology companies are likely to dominate headlines, but next week is also one of the busiest periods so far this earnings season across multiple sectors.

Markets are likely to focus on guidance, margins and capital expenditure as much as the headline results.

Market impact

- Nasdaq leadership breadth may respond to guidance consistency

- With equity markets remaining generally strong, current valuations will again be tested

- Overall performance across sectors will be viewed as a lens into the state of the econ

(Note: Dates may be subject to change)

Gold

At the US close on 22 January 2026, COMEX gold futures traded around US$4,920/oz, with the psychologically important 5,000 level in view.

Sensitivity to Treasury yields and the USD, policy uncertainty, and geopolitical developments may influence price action either way.

Market impact

- Gold prices can remain sensitive to changes in Treasury yields, USD movements and geopolitical developments.

- Movements around record levels can be volatile and unpredictable, and may reverse quickly.

Final takeaways

- If Australian CPI suggests inflation persistence, market pricing may continue to lean toward a February RBA move

- If the Fed narrative is less dovish than expected, current assumptions may be challenged

- If mega-cap earnings reinforce valuation confidence, leadership from these stocks may help support broader equity levels

- If gold holds near record highs, USD weakness and hedging demand may remain key drivers

US earnings season is where the market gets its cleanest burst of new information. For Australians, it usually lands while the country is asleep. This is not just “US company news”. It is the scoreboard for the Nasdaq, the S&P 500, and risk appetite more broadly, with spillover into SPI futures, the AUD, and sector mood at the ASX open.

What this guide covers

- The four-wave rhythm (why volatility clusters in predictable months)

- The order of play (banks → tech → retailers) and what each group tends to reveal

- Before market open (BMO) vs after market close (AMC)

- The few lines markets care about (surprise vs expectations, and the forward reset)

- How earnings information can flow through to Australia via futures, FX, and sector sentiment

US earnings season basics

Earnings season is the 4 to 6-week window after each quarter when most US-listed companies report a new set of numbers and a new story.

Calendar rhythm and clustering

Earnings does not arrive as a smooth drip. It typically arrives in four recurring waves. Most US reporting clusters around January, April, July, and October. Each wave covers the prior quarter, which is why markets spend the lead-up period building expectations, then reprice quickly as numbers and guidance hit.

The sequence is familiar: banks open, tech dominates the middle, retailers close. That order matters because each group updates a different part of the macro story. If you only track one set of reports, make it the Magnificent 7 — here’s the Mag 7 earnings calendar for 2026 (Aussie-friendly timing)

.png)

Time zones: the two windows

For Australians, the key is when the first move hits.

- AMC (after market close): often Sydney and Melbourne morning, sometimes near the ASX open

- BMO (before market open): often late night, with the initial reaction while Australia sleeps

Daylight saving shifts timings, but the structure is consistent: two windows, two different liquidity conditions.

How the market digests an earnings event

Earnings is rarely a single reaction. It is a sequence.

- Headline release (EPS and revenue versus consensus)

- Immediate price discovery (often in after-hours or pre-market liquidity)

- Call and Q&A (guidance, margins, and demand tone get tested)

- Next US cash session (follow-through, reversals, broader positioning)

- Australia opens into the aftershock (futures, FX, and sector mood already set)

Translation: volatility often clusters around reporting windows because the calendar can concentrate new information and repricing.

Expectations: the scoreboard the market uses

Markets do not price “good” or “bad” in isolation. They price the gap versus expectations, then adjust the forward story. That is why the same quarter can look strong on paper and still disappoint if it lands below what the market had already baked in.

Most headlines boil down to three checks. First, actual results versus consensus. Second, actual results versus what the company previously guided. Third, quality and durability. That tends to show up in margins, the mix across segments, and whether cash flow backs up the earnings number.

Guidance: the forward reset

Guidance is where the narrative can change without the quarter changing. A company can deliver the past cleanly, then move the goalposts for what comes next. That forward reset is often what drives the bigger repricing.

In practice, guidance usually lands in a few buckets. Revenue or EPS outlook sets the top-line and earnings path. Margin outlook tells you how confident management is about costs and pricing. Capex language signals how heavy the investment cycle is likely to be. Capital return talk, including buybacks, is a read on balance sheet posture and priorities.

Translation: markets trade forward narratives. Guidance is the mechanism.

The call: where tone becomes data

Prepared remarks are polished. The call is where the market stress-tests the story. The Q&A is where the edges show up, because that is where analysts push on the parts that matter and management has to answer in real time.

Listen for the tells. Demand language can shift from broad to patchy. Pricing can move from power to pressure. Margin confidence can sound steady or start to carry caveats. And the “we are not breaking that out” moments matter too. What management avoids can be as informative as what it highlights.

Key takeaways

- Earnings season clusters in four waves (January, April, July, October), so volatility often arrives in blocks.

- The sequence matters. Banks open the read on confidence, tech steers index tone, retailers often close the consumer chapter.

- From Australia, BMO and AMC are the two windows that shape what you wake up to.

- Markets trade surprise vs expectations, then the forward reset via guidance and call tone.

- The spillover typically shows up through futures, FX, and sector sentiment before the ASX open.

Glossary (quick definitions)

- EPS: earnings per share

- Consensus: the market’s compiled estimate set

- Guidance: management’s forward-looking outlook ranges/comments

- Margins: profitability as a percentage of revenue

- Capex: capital expenditure (investment spend)

- BMO/AMC: before market open / after market close (US reporting labels)

- After-hours / pre-market: trading sessions outside regular US cash hours

- Correlation: how tightly assets move together (often rises in macro or de-risking periods)

As geopolitical narratives continue to simmer, US and European markets move into the rest of the week with three dominant drivers: US inflation data, the start of US earnings season, and an unusual Fed-independence headline risk after the DOJ subpoenaed the Federal Reserve.

Quick facts:

- US consumer price index (CPI) and producer price index (PPI) are the key macro releases and are likely to impact the US dollar (USD) and other asset classes if there is a significant move from expectations.

- JPMorgan reports Tuesday, with other major US banks through the week, as the Q4 reporting season gets underway.

- Reporting around DOJ action involving the Fed, and Chair Powell’s prior testimony, created early market volatility on Monday, with markets sensitive to anything that may be perceived as undermining Fed independence.

- President Trump announced this morning that any country doing business with Iran will face a 25% tariff on all business with the US, effective immediately.

- Europe’s production and growth updates, including Eurozone industrial production and UK monthly GDP and trade data, are later in the week.

United States: CPI, Fed path, DOJ and Fed headline risk, and banks leading earnings

What to watch:

The US is carrying the highest event density in global data releases this week. CPI and PPI will both be watched for moves away from expectations.

Any meaningful surprise can shift Fed policy expectations. Markets are currently pricing a lower likelihood of a March rate cut (under 30%) than this time last week, based on fed funds futures probabilities tracked by CME FedWatch.

Bank earnings may set the tone for the reporting season as a whole. Forward guidance is likely to be as important as Q4 performance, with valuations thought to be high after another record close in the S&P 500 overnight.

Key releases and events:

- Tue 13 Jan (Wed am AEDT): CPI (Dec) (high sensitivity)

- Tue 13 Jan (Wed am AEDT): JPMorgan earnings before market open (high sensitivity for banks and risk tone)

- Wed to Thu: additional large-bank earnings cluster (high sensitivity for financials sentiment)

- Wed 14 Jan (Thu am AEDT): US PPI

- Thu 15 Jan (Fri am AEDT): US weekly unemployment

- Throughout the week: Fed member speeches

How markets may respond:

S&P 500 and US risk tone: US indices are near record levels. The S&P 500 closed at 6,977.27 on Monday. Hotter-than-expected inflation can pressure growth and small-cap equities in particular, and weigh on the market broadly. Softer inflation can support further risk-on behaviour.

USD: Inflation data is the obvious driver this week for the greenback, but any continuation of DOJ and Fed developments, or geopolitical escalation, may introduce additional USD influences.

With the USD testing the highest levels seen in a month, followed by some light selling yesterday, some volatility looks likely. Gold has also been bid as a potential safety trade and hit fresh highs in the latest session, suggesting demand for defensive exposure remains present.

Earnings (banks): In a market already priced near highs, results can still create volatility if they are not accompanied by supportive earnings per share (EPS), revenue and forward guidance. Financials will likely see the first-order response, but any early pattern in results and guidance can influence the broader market beyond the first few days.

UK and Eurozone: growth data influence amid continuing equity strength

What to watch:

In a week where Europe may be driven primarily by events in the US and geopolitical narrative, the Eurozone industrial production print is still a noteworthy local release.

In the UK, monthly GDP and trade numbers on Thursday may influence both the FTSE 100 and the pound, particularly if there is any meaningful surprise.

Key releases and events:

Eurozone

- Wed 14 Jan: Eurozone industrial production (Nov 2025) (medium sensitivity for cyclical sectors)

UK

- Thu 15 Jan: GDP monthly estimate (Nov 2025) (high sensitivity for GBP and UK rate expectations)

- Thu 15 Jan: UK trade (Nov 2025) (low to medium sensitivity)

How markets may respond:

EUR spillover from the US: Despite light Eurozone data, the US response is likely to matter most this week, with the US dollar index a major driver of broader G10 FX direction.

DAX (DE40): Germany’s index is also trading at or near record levels and closed at 25,405 on Monday. (2) If the index is extended, it may react more to global rate moves and shifts in perceived risk.

FTSE 100 and GBP: The FTSE hit a new high in the overnight session, driven particularly by materials and mining stocks. (5) Any GDP surprise can re-price GBP and UK equities quickly in an environment where growth concerns persist.

US and Europe calendar summary (AEDT)

- Wed 14 Jan: US CPI, US bank earnings kick-off (notably JPMorgan)

- Wed 14 Jan: Eurozone industrial production (Nov 2025)

- Thu 15 Jan: UK monthly GDP (Nov 2025) and UK trade (Nov 2025), US bank earnings continue

- Fri 16 Jan: US weekly unemployment, US bank earnings continue

Bottom line

- If US CPI surprises higher, markets may lean toward higher-for-longer interest rate pricing, which can pressure equity multiples and lift rates volatility.

- If bank earnings are solid but guidance is cautious, equities can still see two-way swings given index levels near records and high valuations.

- If DOJ and Fed headlines escalate, they may override normal data reactions to some degree. That could increase demand for perceived safe havens such as gold and lift FX volatility.

- For Europe, Eurozone production (Wed) and UK GDP and trade (Thu) are the key local data. The region is still likely to trade primarily off US outcomes and broader risk sentiment.

So why do Magnificent 7 (Mag 7) earnings matter for Australians? Because the US earnings season is a different sport from Australia, and this is where the scoreboard sits. These seven names do not just report results, they set the tone for the Nasdaq, the S&P 500, and risk appetite more broadly. They often influence index tone, but market moves are not guaranteed and can fade or reverse.

The Aussie edge: time zones, event windows, and what gets priced

For Aussie traders, the challenge is not just timing. It's overnight gaps, liquidity, and AUD/USD currency moves that can amplify or offset the share price reaction.

Most Mag 7 results land after the US close, so the initial move often hits Sydney morning liquidity. Markets may react first to the headline numbers, then again during the call as guidance, margins and capex are digested — but the sequence varies by quarter.

What this guide gives you, company by company

For each company, we map the US Eastern Time (ET) reporting window and the Sydney time window (AEDT), flag whether it is before or after the US close, and narrow the focus to the few drivers that tend to move price.

Apple Inc (NASDAQ: AAPL)

Apple is a “quality” print until it isn’t. The market doesn’t just ask if Apple beat. It asks whether demand and mix support the next leg.

Reporting window (confirmed)

- US reporting time: Thu, 29 Jan 2026 at 5:00 pm ET (after close)

- AU reporting time: Fri, 30 Jan 2026 at 9:00 am AEDT

Quarter snapshot (Q1)

- Projected consensus earnings per share (EPS): US$2.65

- Projected consensus revenue: US$135.86 billion (bn)

- Call focus: iPhone demand and mix, services trajectory, China and FX translation

Translation: Apple “beats” are common. The repricing comes from demand tone and margin language.

Earnings expectations and how the market will frame it

A “beat” means EPS and revenue come in above expectations, but it only really counts if demand still sounds healthy and the gross margin commentary stays straightforward.

A “meet” means results are basically in line, so attention shifts to the call. Investors will focus on iPhone product mix, how fast Services is growing, and whether any specific regions are weakening.

A “miss” often reacts more negatively if it is driven by weaker demand, because the market may treat it as the start of a trend, not a one time issue. You can also see a big price gap right after the report, before the call even starts.

Meta Platforms Inc (NASDAQ: META)

Meta is expected to report the December quarter, which effectively turns this into a Sydney morning catalyst for Aussie traders. The headline move hits first but the second leg often comes from the call, when guidance and capex ranges get priced.

Reporting window (expected)

- US reporting time: Mon, 2 Feb 2026 at 4:05 pm ET (after close)

- AU reporting time: Tue, 3 Feb 2026 at 8:05 am AEDT

Quarter snapshot (Q4)

- Projected consensus EPS: US$8.29

- Projected consensus revenue: US$58.27 bn

- Call focus: AI infrastructure capex, Ads demand plus Reels monetisation and Reality Labs losses versus discipline

Translation: Meta can beat the print and still sell off if the Street hears “higher spend, longer payoff.”

Earnings expectations and how the market will frame it

A “beat” means EPS and revenue come in above consensus, but it only really counts if guidance stays intact and the 2026 capex and expense ranges do not get wider.

A “meet” is close enough that the stock trades the tone of the call: how broad ad demand looks, whether Reels monetisation is improving, and whether spending sounds capped or more open ended.

A “miss” can turn ugly quickly if it comes with weaker ad demand commentary or higher spend bands. With expectations already high, the initial gap can be sharp, and what happens next depends on whether guidance can steady the story.

Alphabet Inc (NASDAQ: GOOGL)

Alphabet is still an ads engine first, and a Cloud and AI story second. The market wants proof that Cloud profitability and AI spend can coexist without compressing the whole narrative.

Reporting window (confirmed)

- US reporting time: Wed, 4 Feb 2026 at 4:00 pm ET (after close)

- AU reporting time: Thu, 5 Feb 2026 at 8:00 am AEDT

Quarter snapshot (Q4)

- Projected consensus EPS: US$2.59

- Projected consensus revenue: TBC

- Call focus: Search and YouTube ads pricing and volume, Cloud growth and profitability, AI capex and monetisation signals

Translation: The market forgives a lot if ads are strong and Cloud margins keep improving.

Earnings expectations and how the market will frame it

A “beat” means EPS and revenue come in above consensus, but it only really matters if ad demand sounds broad and Cloud profitability does not slip while AI spending ramps.

A “meet” puts the call in the driver’s seat, with investors listening for ad pricing trends, YouTube momentum, and whether capex is moving higher.

A “miss” hurts most if it is driven by weaker ads, because then the market starts debating the ad cycle, not just the company.

Amazon.com Inc (NASDAQ: AMZN)

Amazon is two businesses stapled together in the tape. The market uses AWS to price growth and uses retail margins to price discipline.

Reporting window (expected)

- US reporting time: Mon, 2 Feb 2026 at 4:00 pm ET (after close)

- AU reporting time: Tue, 3 Feb 2026 at 8:00 am AEDT

Quarter snapshot (Q4)

- Prijected consensus EPS: US$1.97

- Projected consensus revenue: US$211.33 bn

- Call focus: AWS growth and margins, retail profitability/fulfilment efficiency, advertising momentum, capex tone

Translation: AWS decides the direction. Retail decides the confidence.

Earnings expectations and how the market will frame it

A “beat” means EPS and revenue come in above consensus, but it only really matters if AWS holds steady or speeds up again and management does not worry the Street with spending plans.

A “meet” puts AWS and margin tone front and centre, and the call does most of the work.

A “miss” usually gets hit hardest when AWS growth slows or operating income guidance disappoints, because that is what can reset the whole valuation debate.

Microsoft Corp (NASDAQ: MSFT)

Reporting window (confirmed)

- US reporting time: Wed, 28 Jan 2026 at 4:00 pm ET (after close)

- AU reporting time: Thu, 29 Jan 2026 at 8:00 am AEDT

Quarter snapshot (Q2)

- Projected consensus earnings per share (EPS): US$3.86

- Projected consensus revenue: US$80.09 bn

- Call focus: Azure growth, AI monetisation (Copilot/attach), capex intensity, and margin trajectory

Translation: This is usually a cloud plus capex trade, not an EPS trade.

Earnings expectations and how the market will frame it

A “beat” means EPS and revenue come in above consensus, but it only really matters if Azure is holding up and capex does not sound unlimited. Beat plus steady cloud trends and stable margins is the upside script the tape usually rewards.

A “meet” puts the focus on the call, especially Azure growth, commercial bookings tone, and how quickly capex is stepping up.

A “miss” usually gets punished most when cloud growth slows or margins get shaky, because that is the key forward anchor the market leans on.

NVIDIA Corp (NASDAQ: NVDA)

Nvidia is the season’s last boss. Markets treat it like a read-through on AI capex itself. The print matters, but guidance and gross margin are the real price setters.

Reporting window (confirmed)

- US reporting time: Wed, 25 Feb 2026 at 4:20 pm ET (after close)

- AU reporting time: Thu, 26 Feb 2026 at 8:20 am AEDT

Quarter snapshot (Q4)

- Projected consensus EPS: US$1.45

- Projected consensus revenue: US$65.47 bn

- Call focus: Data centre demand versus capacity, gross margin trajectory, supply/lead times, next-quarter guide

Translation: Guidance and gross margin commentary often drive the reaction, but outcomes vary.

Earnings expectations and how the market will frame it

A “beat” means EPS and revenue come in above consensus, but it only really matters if the next quarter outlook confirms demand is still strong and the gross margin message stays solid.

A “meet” means the call becomes the decider, and the stock trades the outlook, margins, and what management says about supply conditions.

A “miss” can gap down fast, especially if it comes with softer forward guidance, because the market may take it as a clue about the broader AI spending cycle.

Tesla Inc (NASDAQ: TSLA)

Tesla’s earnings are rarely just about the quarter. The print hits first, but the real repricing usually happens when the call clarifies margins, demand, and the autonomy timeline. For Aussie traders, it’s a Sydney morning catalyst.

Reporting window (confirmed)

- US reporting time: Wed, 28 Jan 2026 at 4:05 pm ET (after close)

- AU reporting time: Thu, 29 Jan 2026 at 8:05 am AEDT

Quarter snapshot (Q4)

- Projected consensus EPS: US$0.44

- Projected consensus revenue: US$25.15 bn

- Call focus: Autonomy/robotaxi cadence, auto gross margin, pricing/demand and energy storage scale

Translation: Tesla can “beat” and still get sold if margins compress or the roadmap tone shifts.

Earnings expectations and how the market will frame it

A “beat” means EPS and revenue come in above consensus, but it only really matters if the margin story stays intact and management does not add fresh uncertainty around pricing or timing.

A “meet” is close enough that the stock trades the tone of the call, especially on demand, how durable margins look, and progress toward autonomy milestones.

A “miss” gets hit fastest when it comes with weaker margin language or softer demand comments, because the market will assume next quarter looks tougher, not easier.