市場新聞與洞察

透過專家洞察、新聞與技術分析,助你領先市場,制定交易決策。

4月8日宣布的停火以及围绕45天休战的平行讨论并未解决霍尔木兹海峡的混乱问题。目前,他们已经限制了最坏的情况,但油轮运输量仍处于正常水平的一小部分,伊朗对过境费的需求预示着结构性转变,而不是暂时的转变。

最初的地区冲突已成为全球能源冲击,市场面临的问题不再是霍尔木兹是否受到干扰,而是这种混乱对石油的最低定价产生了多大的永久性影响。

关键要点

- 每天约有2000万桶(桶)的石油和石油产品通常通过伊朗和阿曼之间的霍尔木兹海峡,相当于全球石油消费量的约五分之一,约占全球海运石油贸易的30%。

- 这是流量冲击,不是库存问题。石油市场依赖于持续的吞吐量,而不是静态存储。

- 如果中断持续超过几周,布伦特原油可能会从短期飙升转向更广泛的价格冲击,存在滞胀风险。

- 穿越海峡的油轮运输量从每天约135艘下降到中断高峰期的不到15艘船只,减少了约85%,超过150艘船只停泊、改道或延误。

- 4月8日宣布了为期两周的停火,为期45天的休战谈判正在进行之中。伊朗已分别表示要求对使用该海峡的船只收取过境费,如果正式确定,这将是能源成本的永久地缘政治最低标准。

- 市场已经开始从增长和技术敞口转向能源和国防企业,这反映了人们的观点,即石油价格上涨正在成为结构性成本,而不是暂时的风险溢价。

世界上最关键的石油阻塞点

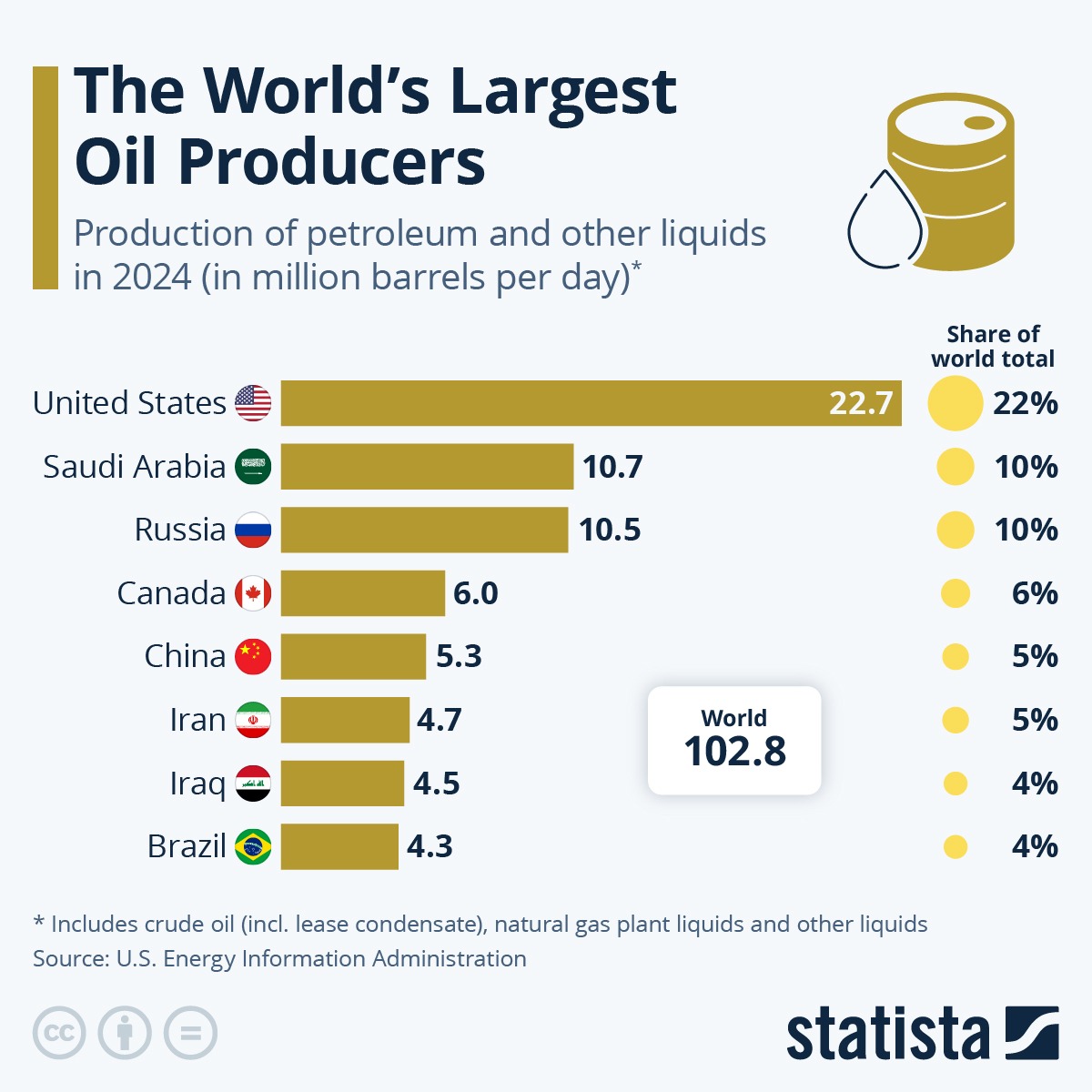

霍尔木兹海峡每天处理大约2000万桶石油和石油产品,相当于全球石油消费量的20%和全球海运石油贸易的30%左右。由于全球石油需求接近1.04亿桶/日,且剩余产能有限,在最近的升级之前,市场已经处于紧密平衡状态。

该海峡也是液化天然气的重要走廊。2024年,平均每天约有2.9亿立方米的液化天然气通过该路线,约占全球液化天然气贸易的20%,亚洲市场是主要目的地。

国际能源署(IEA)将霍尔木兹描述为世界上最重要的石油运输阻塞点,并指出,即使是部分中断也可能引发价格的大幅波动。布伦特原油已跌破每桶100美元,这既反映了物质紧张,也反映了地缘政治风险溢价的上升。

由于流量减慢,油轮处于空转状态

现在,航运和保险数据实时显示压力。据报道,超过85艘大型原油运输船滞留在波斯湾,而由于运营商重新评估安全和保险,有150多艘船舶停泊、改道或延误。据估计,这将使1.2亿至1.5亿桶原油在海上闲置。

这些量仅代表霍尔木兹正常吞吐量的六到七天,或略高于一天的全球石油消费。

最新的航运和保险数据现在证实,有150多艘船只停泊、改道或延误,高于最初报告的85艘船只。闲置原油的1.3天全球消费保障仍然是约束性制约因素:这是流量冲击,不是储存问题,停火尚未转化为产量的实质性恢复。

建立在流量而不是存储基础上的市场

石油市场在持续波动中运作。炼油厂、石化厂和全球供应链经过调整,可以沿着可预测的海道稳定交付。当流经占全球石油消耗量约五分之一和全球海运石油贸易约30%的阻塞点时,该系统可以在几天之内从平衡变为赤字。

剩余产能主要集中在欧佩克内,估计仅为每天300万至500万桶。这远低于霍尔木兹水流受到严重干扰时面临的风险交易量。

Oil market analysis

How long do idle tankers last?

135M idle barrels — days of cover against each demand benchmark

vs. Strait of Hormuz daily flow (20M bbl/day)

vs. Global oil consumption (104M bbl/day)

vs. US Strategic Petroleum Reserve release (1M bbl/day)

135M

idle barrels on tankers (midpoint of 120–150M range)

~33%

of daily Hormuz flow that is idle storage, not transit

<31 hrs

is all idle storage against global daily consumption

通货膨胀风险和宏观溢出效应

石油冲击的通货膨胀影响通常以波浪形式出现。随着汽油、柴油和电力成本的上涨,燃料和能源价格的上涨可能会迅速提振总体通货膨胀。

随着时间的推移,更高的能源成本可能会流向货运、食品、制造业和服务业。如果混乱持续下去,通货膨胀率上升和增长放缓相结合,可能会增加滞胀环境的风险,使中央银行面临艰难的权衡。

不容易抵消,系统几乎没有松弛

当前局势之所以特别严重,是因为全球体系缺乏松弛。

当处理近2,000万桶/日(约占全球石油消耗量的五分之一)的阻塞点受到损害时,将近1.03亿至1.04亿桶的全球供需几乎没有备用缓冲。估计每天300万至500万桶的剩余产能,主要在欧佩克内部,只能覆盖风险产量的一小部分。

替代路线,包括绕过霍尔木兹的管道和改道运输,只能部分抵消流量的损失,而且通常成本更高,交货时间更长。

底线

在霍尔木兹海峡的过境恢复并被视为可靠安全之前,全球石油流动可能继续受损,风险溢价上升。对于投资者、政策制定者和企业决策者来说,核心问题是石油能否每天不间断地转移到需要去的地方。

Venezuela commands the world's largest proven oil reserves at 303 billion barrels. Yet political turmoil, global sanctions, and recent US intervention show that being the biggest isn’t always best.

Quick facts:

- Venezuela holds 18% of the world's total proven oil reserves despite producing less than 1% of global consumption.

- Just four countries (Venezuela, Saudi Arabia, Iran, and Canada) control over half the planet's proven reserves.

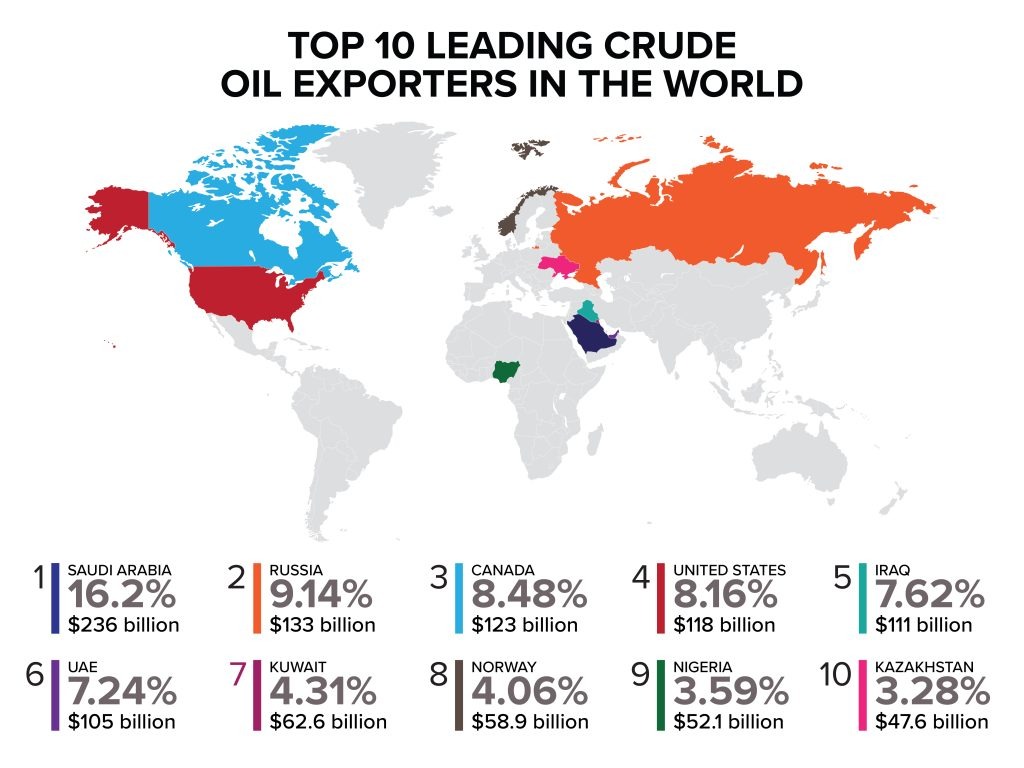

- Saudi Arabia dominates crude oil production contributing to over 16% of global exports.

- US shale technology has enabled America to lead in production despite ranking ninth in reserves.

Top 10 countries by proven oil reserves

1. Venezuela – 303 billion barrels

- Controls 18% of global reserves, primarily extra-heavy crude in the Orinoco Belt requiring specialised refining.

- Heavy crude trades $15-20 below Brent benchmarks due to high sulphur content and complex processing requirements.

- Output crashed 60% from 2.5 million bpd in 2014 to less than 1.0 million bpd last year.

- Approximately 80% of exports flow to China as loan repayment, with export revenues dwarfed by reserve potential.

2. Saudi Arabia – 267 billion barrels

- Majority light, sweet crude oil requires minimal refining and commands premium prices, contributing to world-leading exports of $191.1 billion in 2024.

- Maintains 2-3 million bpd of spare production capacity, providing market stabilisation capability during supply disruptions.

- Oil comprises roughly 50% of the country’s GDP and 70% of its export earnings.

- Production decisions significantly impact international oil prices due to market dominance.

3. Iran – 209 billion barrels

- Heavy Western sanctions severely limit the country’s ability to monetise and access international markets.

- Production estimates vary significantly (2.5-3.8 million bpd) due to sanctions, limited transparency, and restricted international reporting.

- Significant crude volumes flow to China through discount arrangements and sanctions-evading mechanisms.

- Sanctions relief could rapidly boost production toward 4-5 million bpd, though domestic consumption (12th globally) reduces export potential.

4. Canada – 163 billion barrels

- Approximately 97% of reserves are oil sands (bitumen) requiring steam-assisted extraction and significant upfront capital investment.

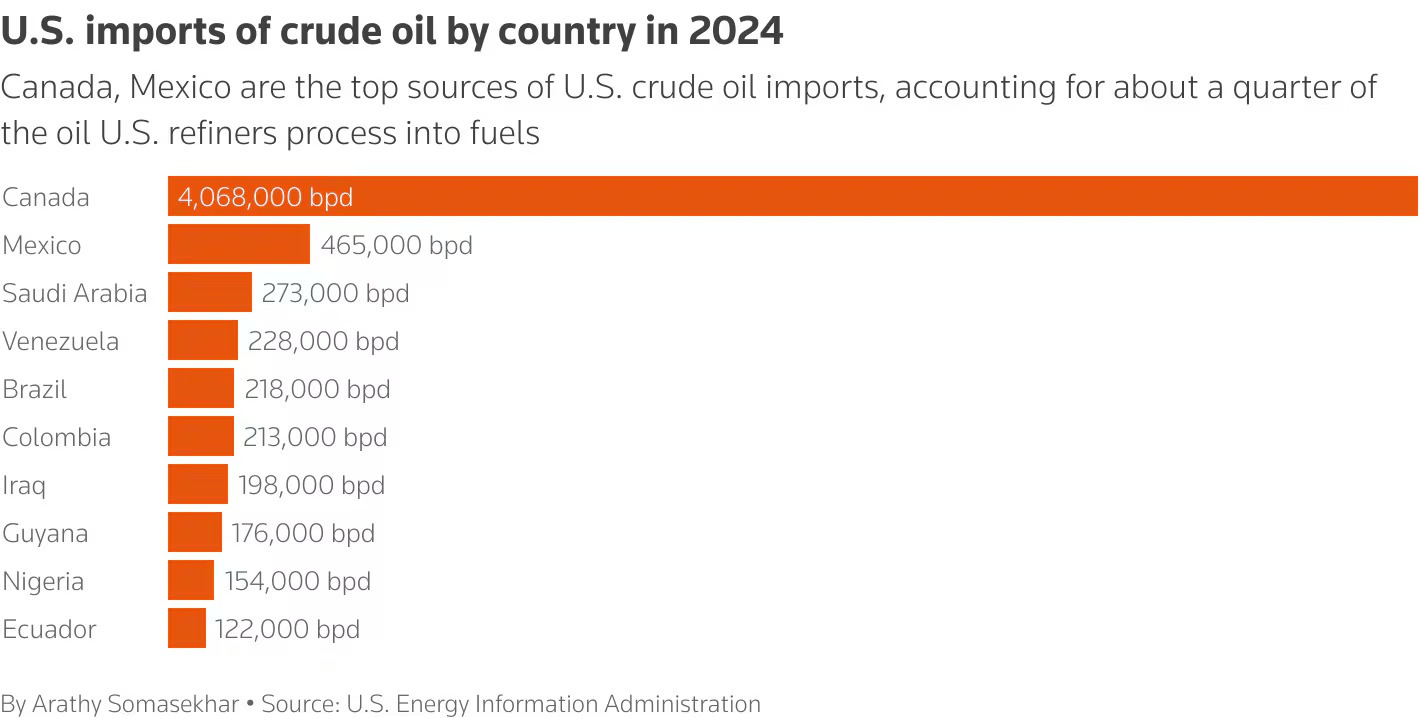

- Political stability and regulatory frameworks position Canada as a secure source compared to volatile producers, with direct pipeline access to US refineries.

- Supplied over 60% of U.S. crude oil imports in 2024, making Canada America's top source by far.

5. Iraq – 145 billion barrels

- Decades of war and sanctions have prevented optimal field development and infrastructure modernisation.

- Improved security conditions since 2017 have enabled production recovery, but pipeline attacks and aging facilities continue to constrain output.

- Oil revenue comprises over 90% of government income, creating extreme fiscal vulnerability.

- Exports flow primarily to China, India, and Asian buyers seeking a reliable Middle Eastern supply, with most production from super-giant southern fields near Basra.

6. United Arab Emirates – 113 billion barrels

- Produces primarily medium-to-light sweet crude commanding premium prices, ranking fourth globally in export value at $87.6 billion.

- Has successfully diversified its economy through tourism, finance, and trade, reducing oil's GDP share compared to Gulf peers.

- Strategic location near the Strait of Hormuz and openness to international oil companies help facilitate efficient global distribution.

7. Kuwait – 101.5 billion barrels

- Reserves are concentrated in aging super-giant fields like Burgan, which require enhanced recovery techniques.

- Favourable geology enables extraction costs around $8-10 per barrel, with proven reserves providing 80+ years of supply at current production rates.

- Oil comprises 60% of GDP and over 95% of export revenue.

8. Russia – 80 billion barrels

- World's third-largest producer despite ranking eighth in reserves.

- Post-2022 Western sanctions redirected crude flows from Europe to Asia, with China and India now absorbing the majority at discounted prices.

- Despite export restrictions and G7 price cap at $60/barrel, it posted the second-highest global export value at $169.7 billion in 2024.

- Russian Urals crude typically trades $15-30 below Brent due to quality, sanctions, and logistics, with November 2024 revenues declining to $11 billion.

9. United States – 74.4 billion barrels

- The shale revolution through horizontal drilling and hydraulic fracturing has made the U.S. the world's #1 oil producer despite holding only the 9th-largest reserves.

- The Permian Basin accounts for nearly 50% of production, with shale/tight oil representing 65% of total output.

- Achieved net petroleum exporter status in 2020 for the first time since 1949, with crude exports growing from near-zero in 2015 to over 4 million bpd in 2024.

- The U.S. government maintains a 375+ million barrel strategic reserve.

10. Libya – 48.4 billion barrels

- Holds Africa's largest proven oil reserves at 48.4 billion barrels, producing light sweet crude commanding premium prices.

- Rival bordering governments compete for oil revenue control, causing production to fluctuate based on political conditions.

- Oil facilities face blockades, militia attacks, and political leverage tactics, preventing consistent returns.

- Favourable geology enables extraction costs around $10-15 per barrel, with geographic proximity making Libya a natural supplier to European refineries.

What does this mean for oil markets?

The concentration of reserves among OPEC members (60% of the global total) ensures the organisation has continued influence over pricing, even as US shale provides a production counterweight.

Venezuela's potential return as a major exporter post-U.S. occupation could eventually ease supply constraints, though most analysts view significant production increases as years away.

Sanctions could create a situation where discounted crude seeks buyers willing to navigate compliance risks. Refiners with heavy crude processing capability may benefit from price differentials if Venezuelan barrels increase.

While reserves appear abundant, economically recoverable volumes depend on sustained high prices. If renewable adoption accelerates and demand peaks sooner than projected, stranded assets become a material risk for reserve-heavy producers.

Global markets are calm but alert in response to the US–Venezuela situation, with US and European equities holding near or testing record levels.

Gains in energy, defence and materials suggest selective positioning. Modest strength in gold and lower yields is indicative of hedging rather than market fear, with oil prices remaining muted.

Quick facts

- US and European equity indices are holding near record highs despite geopolitical headlines. Volatility remains low through the trading session.

- Energy and defence stocks are leading gains, with materials stocks responding to mild gains in previous metals, reflecting selective risk positioning.

- Gold is edging higher, and government bond yields have dipped slightly, signalling mild hedging.

- Oil prices remain range-bound, suggesting no immediate supply shock is being priced in.

- Markets could be sensitive to further geopolitical developments, with any escalation a major potential risk to sentiment.

US–Venezuela tensions escalation has prompted heightened geopolitical scrutiny across the globe, not only related to this action itself but other geopolitical longer-term implications.

There has been a muted and measured response across global financial markets so far, with little significant negative impact evident for now.

Some sectors have had noteworthy gains, whilst the impact on other asset classes has again been calm.

US equities

What’s happening:

US equity markets are showing resilience, with the S&P 500 holding near recent highs and the Dow Jones Industrial Average up 1.23%, pushing into fresh record territory.

What to watch:

- If US indices continue to hold above recent breakout levels, then markets are reinforcing the view that geopolitical risk remains manageable.

- Rising volatility, if seen in the VIX index, may indicate that sentiment may be shifting from selective risk-taking to broader caution.

European equities

What’s happening:

European markets are modestly higher, with the DAX trading at record levels and the FTSE 100 closing over 10,000 for the first time.

What to watch:

- For now, European indices appear to be tracking US strength, suggesting investors are viewing the event as externally contained. Similar sectors are performing well, as seen in overnight US equity performance.

- It is unlikely that we will see any specific regional response, though tensions related to the US administration's narrative around Greenland is noteworthy.

Specific sector moves

Energy stocks

What’s happening:

Energy stocks are leading equity gains across the US (e.g. Chevron Corp – CVX up 5.1%), and European markets, with the potential for increased influence in Venezuela of US oil companies.

What to watch:

- While energy equities outperform while oil prices remain range-bound, then markets are pricing geopolitical caution rather than immediate disruption. If this is accompanied by a rise in crude prices rise together, then it may be indicative of supply risk

Defence stocks

What’s happening:

Defence stocks are attracting some investor interest. (E.g. Lockheed Martin – LMT up 2.92%, General Dynamics – GD up 3.54%).

What to watch:

- Continued outperformance with other sector equity drawdowns may be indicative of some escalation concerns.

Materials & miners

What’s happening:

Materials and mining stocks are finding support alongside modest gains in precious metals and record highs in copper. The S&P Metals & Mining ETF – XME closed 3.28% up.

What to watch:

- Ongoing materials strength alongside stable growth indicators, then the current move may reflect real-asset demand rather than simply a hedging approach. If gold accelerates higher while base metals fail to follow, then investor defensive positioning may be overtaking confidence in growth.

Crude oil

What’s happening:

Oil prices remain subdued, with the futures trading at $58.40, within recent ranges, despite the unfolding geopolitical situation.

What to watch:

- Venezuelan influence on global oil production is not substantial enough on its own to create any major issues in the short term with global oil supply at high levels.

- As a result, the impact is more likely to remain muted, but any significant rises in oil price across multiple sessions may be indicative of some market concerns related to increases in geopolitical-influenced supply expectations.

Gold

What’s happening:

Gold prices are currently edging higher towards all-time highs, reflecting a modest safe-haven play. The closing price for Gold futures is $4454, breaching the psychologically important $4400.

What to watch:

- If gold continues to rise gradually while equities remain firm, then the move reflects a standard hedging approach to assets rather than fear.

- A spike in gold price alongside falling equities and rising volatility, maybe a signal that market risk may be increasing.

Treasury yields

What’s happening:

Yields have eased slightly, indicating a potential selective defensive positioning in asset choice by institutional investors. (10-year Treasury yields at 4.153%, down 0.36%)

What to watch:

- If yields should fall sharply alongside equity weakness, then markets may be shifting toward a risk-off approach.

What to watch next

- If asset-class correlations remain contained, then markets are maintaining confidence in the broader macro backdrop.

- If tensions escalate into broader regional instability or prolonged policy responses, Sharp movements across equities, bonds, and commodities may signify a reassessment of risk.

- If geopolitical developments fail to translate into sustained price dislocation, then the current response is likely to fade.

(All prices quoted correct as of 4.30pm NY time after market close).

.jpg)

January’s market action often matters more than simply marking the opening of the calendar year. Institutional positioning resets, testing of economic assumptions, and early price moves reflect how market participants interpret the first meaningful signals of the year.

While January rarely determines full-year outcomes, it frequently shapes the narratives markets carry into the first quarter (Q1).

Four critical levers: growth, labour, inflation, and policy, can provide an early indication of how markets are processing and prioritising incoming information.

Growth: manufacturing PMIs

January’s first growth test comes from the manufacturing surveys, with markets watching whether signals from S&P Global Manufacturing PMI and ISM Manufacturing PMI tell a consistent story.

Key dates:

- ISM Manufacturing PMI: 5 January, 10:00 AM (ET)/ 6 January, 1:00 AM (AEDT)

What markets look for:

Attention often centres on new orders as a forward-looking indicator of demand, alongside prices paid for early insight into cost pressures.

Broad strength across both surveys would support the narrative that the growth momentum seen toward the end of 2025 may extend into early 2026, easing some concerns about a sharper slowdown. Weaker or conflicting readings would keep the growth outlook uncertain, rather than decisively negative.

How it tends to show up in markets:

Firmer growth signals often appear first in higher short-dated Treasury yields. Rising yields can tighten financial conditions, weigh on equity valuations, and support the USD, with spillover effects across foreign exchange (FX) and commodity markets.

Labour: job openings and payrolls

While early-January Non-Farm Payrolls (NFP) often drive short-term volatility, JOLTS job openings may be more influential in shaping January’s policy narrative.

Key dates:

- JOLTS Job Openings: 7 January, 10:00 AM (ET)/ 8 January, 1:00 AM (AEDT)

- Non-Farm Payrolls (NFP): 9 January, 8:30 AM (ET)/ 10 January, 12:30 AM (AEDT)

What markets look for:

Markets often treat JOLTS as a clearer indicator of underlying labour demand than month-to-month hiring flows.

A continued drift lower in openings would support the view that labour demand is easing in an orderly way, reinforcing confidence that inflation pressures can continue to moderate. A rebound or stalled decline would suggest labour conditions remain firmer than expected.

Market sensitivities:

For markets, easing labour demand typically supports lower short-dated yields and a softer USD, while persistent tightness can push yields higher, strengthen the USD, and increase volatility across rate-sensitive assets.

Inflation: PPI and CPI

Key Dates:

- PPI: 14 January, 8:30 AM (ET)/ 15 January, 12:30 AM (AEDT)

- CPI (December 2025 data): 15 January, 8:30 AM (ET)/ 16 January, 12:30 AM (AEDT)

The inflation signal can be read as a pipeline from producer prices to consumer inflation. Markets are watching whether producer-level cost pressures continue to fade or begin to re-emerge.

What markets look for:

Core PPI, particularly services-linked components, provides an early indication of cost momentum. Core CPI breadth may help determine whether inflation is continuing to cool or showing signs of persistence.

A softer pipeline would reinforce confidence that disinflation can extend into early 2026, increasing the scope for a potential March policy adjustment. Stickier CPI readings above 3% would raise questions about the durability of recent progress.

How rates and the USD often react

Market reaction tends to be led by yields. Cooling inflation pressure usually pulls short-dated yields lower and softens the USD, while persistent inflation risks can push yields higher and tighten financial conditions.

Policy: January FOMC meeting

By the time the Federal Reserve meets at the end of January, markets will have processed the early growth, labour, and inflation signals of the year.

Key Dates:

- FOMC rate decision: 29 January, 2:00 PM (ET)/ 30 January, 6:00 AM (AEDT)

What markets look for:

A policy change is unlikely this month, but how those signals are framed in the statement and press conference still matters. With January cut expectations priced well below 20%, attention is on whether expectations for a March move, currently around 50%, begin to shift.

Confidence that inflation and labour pressures are easing would typically support lower yields and a softer USD. A more cautious tone could lift yields, strengthen the USD, and tighten global financial conditions.

Putting it all together

January’s data acts as condition-setters rather than decision points. The practical takeaway lies in how markets respond as those conditions become clearer:

If growth and labour soften while inflation continues to ease, markets may lean toward a more constructive risk backdrop, with Treasury yields remaining the key guide and expectations for policy easing later in Q1 firming.

If growth holds up and inflation proves sticky, a more cautious posture may be warranted, with heightened sensitivity to Treasury yields, USD strength, and pressure on equity valuations and rate-sensitive commodities.

In 2025, the S&P 500 traded around 6,835 and was up approximately 16% year to date (YTD). Market direction remained most sensitive to Federal Reserve expectations, inflation data and the earnings outlook, with returns also shaped by mega-cap tech leadership and the broader AI narrative. The index pulled back from earlier December highs, but it has so far held above key major moving averages (MA).

Key 2025 drivers included:

- Fed expectations and inflation: Inflation cooled through the year but remained sticky around 2.5% to 3%. A Fed easing bias likely supported price to earnings (P/E) multiples and “risk-on” positioning. More recently, markets appeared increasingly rate-sensitive, with the decreased likelihood of an additional rate cut until March 2026.

- Earnings and guidance: Corporate earnings remained strong quarter on quarter. Recent Q3 results reportedly saw over 80% of the S&P 500 beat earnings per share (EPS) expectations. For Q4, the estimated year-over-year earnings growth rate is 8.1%, despite ongoing concerns around import tariffs and potential margin pressure.

- Index leadership and breadth: Returns were heavily influenced by mega-cap tech and AI beneficiaries, even as broader market breadth appeared less consistent at points through the year.

- Policy headlines and volatility: Trade and tariff headlines drove sharp moves, particularly earlier in the year. Some investors pointed to the “TACO” trade, with rapid recoveries after policy proposals were softened. Over time, similar shocks appeared to have less impact as the market became somewhat desensitised.

- Valuations and sensitivity: The forward 12-month P/E ratio for the S&P 500 is 22, above the 5-year average (20.0) and above the 10-year average (18.7). That gap kept valuation sensitivity, especially in AI-linked names, firmly in focus.

Current state

The S&P 500 is about 1% below record highs hit earlier in December. That could indicate the broader uptrend remains in place, with a move back toward the recent highs one possible scenario if momentum improves. Despite the recent retracement, the index remains above all key major moving averages (MA). The latest bounce followed lower than expected CPI numbers earlier this week, alongside continued, and to some, surprising optimism about what may come next.

What to watch in January

- Q4 earnings from mid-January: Results and guidance may help clarify whether valuations are being supported by forward expectations.

- AI narrative and positioning: With AI-linked mega-caps carrying a large share of market capitalisation, changes in sentiment or expectations could have an outsized impact on index performance.

- US jobs and CPI data: The latest US jobs report reportedly points to the highest headline unemployment rate since 2021. Cooling inflation this week may keep markets alert to shifts in rate cut timing, particularly around the March decision.

S&P 500 daily chart

Major FX pairs

AUD/USD

AUD/USD has been choppy in 2025. Since the “redemption day” drop in April, the move has looked more like a steady grind higher than a clean upside trend.

Key levels

Recent peaks in early September and mid-December highlight resistance near 0.6625. Support has been evident around 0.6425, where price bounced over the last month.

What is supporting the bounce

That support test coincided with stronger than expected jobs and inflation data, lifting expectations that the Reserve Bank of Australia (RBA) may raise rates during 2026 rather than cut again. The latest pullback looks contained so far, with buying interest already visible and price still above key longer-term moving averages.

What could drive a breakout

The pair remains range-bound, but the tilt is still constructive. If Chinese data stays firm, metals prices hold up, and the central bank outlook remains relatively hawkish, a break above resistance could gain more traction.

AUD/USD daily chart

EUR/USD

After early 2025 euro strength, EUR/USD has mostly consolidated since June in a roughly 270 pip range. This month tested 1.18 resistance, reaching highs not seen since September.

What price is doing now

The recent pullback still lacks strong downside conviction. Some technical analysts refer to the 1.17 area as a near-term reference level.

What could come next

If price holds 1.17 and buyers step back in, another push toward 1.18 is possible. One view is that the European Central Bank (ECB) could be less inclined to ease in 2026, which could be consistent with a firmer EUR/USD scenario. Broader analyst commentary also suggests the euro may stall rather than collapse against the US dollar, although outcomes remain data and policy dependent.

EUR/USD daily chart

USD/JPY

Year-to-date picture

USD/JPY is close to flat overall for the year. After US dollar weakness in Q1, the pair reversed higher and now sits just below resistance near 158.

Rates remain the main driver

Rate differentials still favour the US dollar. The Bank of Japan (BOJ) held steady for much of the period despite expectations it might act, and the recent rate increase was modest. Policy has only moved marginally away from zero.

What could shift the balance

Rate differentials remain a key influence. Without a clearer shift in BOJ policy, the JPY may find it difficult to sustain a rebound. Some market commentators cite 154.20 as a chart reference level.

USD/JPY daily chart

.jpg)

Markets have bounced back strongly this week. The S&P 500 is now just 1.5% from record highs, and the Nasdaq is recovering well following its pullback.

Rate Cut Expectations

The main driver behind this rally was a shift in Federal Reserve rate cut expectations. Markets are currently pricing in a quarter-point rate cut for December, with only a 25% chance of another reduction in January. This week's economic data will be crucial in shaping expectations going into 2026.

Key Economic Data This Week

Several important data releases are scheduled for this week. The PCE inflation data — the Fed's preferred inflation measure — for September will finally be released on Friday and could have the biggest impact on December and January rate decisions. The ADP jobs report and weekly jobless claims will also be released, while the non-farm payrolls report has been delayed again.

Global Manufacturing Snapshot

Today also kicks off a busy week of manufacturing data releases. Global PMI numbers are due across the board, including figures from the Eurozone, UK, Germany, and the US this evening. These reports will provide a critical snapshot of global economic health and could help reveal the impact of the US trade tariffs.

Gold Breaks Higher

Gold made a significant move on Friday, breaching the key $4,200 level after consolidating last week. The precious metal has followed through today, and the $4,400 level now looks achievable if buying pressure continues.

Bitcoin Under Pressure

Bitcoin has given up last week's modest gains and seen substantial selling pressure. A significant drop of about $4,000 occurred during Asian trading this morning — a notable decline for an Asia session. The key level to watch is $84,000, with potential support at $80,000 (the lowest level since March).

Market Insights

Watch Mike Smith's analysis of the week ahead in markets.

Key Economic Events

Stay up to date with the key economic events for the week.

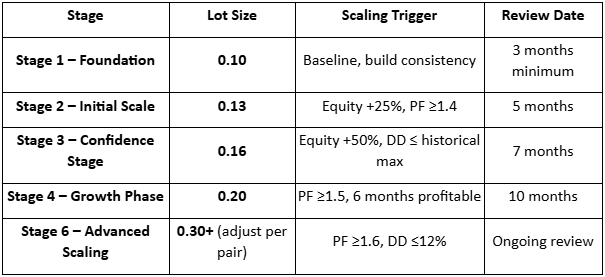

The decision to scale (increase the traded lot size of a specific EA) should be based on statistical evidence that indicates your EA has the potential to perform to certain expectations.

Equal weight should be given to the decision to scale, as to the initial decision to deploy an EA. This guide provides an indicative approach on how to put together and action your scaling plan.

Before You Start Your Scaling Plan

Important: this should be an individual plan that is consistent with your personal trading objectives, your EA portfolio, and your personal financial situation (including account size).

We are going to use a starting lot of 0.10 per trade in the examples in this document —you want to adjust this based on your own risk tolerance.

Whatever your chosen lot size start point, EA scaling should be a pre-planned incremental approach, scaling stepwise based on performance metrics you are seeing in your live trading account.

You should also have assessed the current margin usage of your EA portfolio exposure to ensure that any scaling and related increased margin requirements are appropriate to the size of your account.

Suggested Scaling Baseline Requirements

Scaling should only be performed when your EA is performing to what you deem to be a good standard. To make this judgment, you need to set some minimum performance standards.

The past performance of your EA is not a guarantee of future performance. If market conditions change, you must remain vigilant and continue to measure performance on an ongoing basis for every live EA you have.

You need to define the key metrics that are important to you.

Two important metrics to include are:

- The number of trades: to provide some evidence of reliability

- The period of time: to have had exposure to at least some variation in market conditions

Example of how you may lay your metrics out in a table:

Some may choose to include proximity to original expectations of other metrics, such as minimum win rate, average profit in winning trades, and average loss in those that go against you.

It should only be after your metrics are met that lot scaling begins on any specific EA.

Lot Size Scaling Ladder

Below is an example of a performance-based scaling plan assuming a 0.10-lot baseline.

Again, this is indicative. It provides a framework with clear review dates and an approach that illustrates incremental scaling. You must still define a regime that is right for your specific trading objectives.

Risk Guardrails

It is vital to keep an eye on your general account risks and have limits in place that guide your EA use.

Such limits must be constant across all stages of scaling and referenced beyond the risk of a single EA, but to your portfolio as a whole.:

Per-Trade Risk (Nominal)

Trade risk for any one trade should be seen in the context of account size and the dollar risk based on the risk parameters you have set for your EA.

Specify a maximum percentage of the account balance — a $200 loss is more impactful on a $1000 account compared to a $10,000 account.

Stick to what is right for you in terms of your tolerable risk level based on your trading objectives and financial situation. A common suggestion is a 1-2% risk of account equity per trade.

Total Open Exposure

Specifying maximum exposure in the number of EAs open at any time and those that use the same asset class is important for overall portfolio risk management.

There are tools you can use to monitor exposure risk generally, as well as those that can be used to indicate single asset exposure.

Margin Usage

It is always desirable that your set exit approaches and parameter levels are what your exits are based on. It should not be because your margin usage has meant you have moved into a margin call situation.

Specify a minimum level to adhere to and make sure that your account is sufficiently funded. If volatility or slippage rises (e.g., news events or illiquid sessions), reduce lot size temporarily.

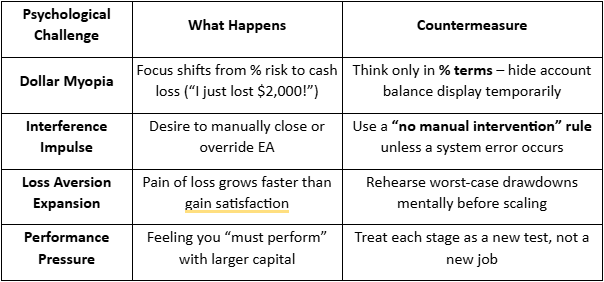

Scaling Psychology – Managing “Big Numbers”

As lot sizes rise, your emotions may respond accordingly when you see the larger dollar amounts that your EA is generating.

If you are used to seeing an average profit of $100 and average loss of $50, and suddenly you are seeing significantly bigger numbers, it creates an emotional challenge where you may be tempted to do a “discretionary override”.

Although there are situations, such as major market events, overexposure in a specific asset, or VPS or account system problems, where such intervention may be considered, generally this would distort the actual performance evaluation of your EA and is not encouraged (unless it is pre-planned).

The table below presents some of the generally accepted challenges and offers suggestions on how to manage them.

Your Plan Into Action…

In practical terms, your scaling plan should have two components:

- The key parameters for action on your chosen key metrics

- Specified periodic review times to make your next scaling decision

This is not a race. Having systems in place facilitates creating the opportunity that scaling brings while still mitigating the risks.