市場新聞與洞察

透過專家洞察、新聞與技術分析,助你領先市場,制定交易決策。

4月8日宣布的停火以及围绕45天休战的平行讨论并未解决霍尔木兹海峡的混乱问题。目前,他们已经限制了最坏的情况,但油轮运输量仍处于正常水平的一小部分,伊朗对过境费的需求预示着结构性转变,而不是暂时的转变。

最初的地区冲突已成为全球能源冲击,市场面临的问题不再是霍尔木兹是否受到干扰,而是这种混乱对石油的最低定价产生了多大的永久性影响。

关键要点

- 每天约有2000万桶(桶)的石油和石油产品通常通过伊朗和阿曼之间的霍尔木兹海峡,相当于全球石油消费量的约五分之一,约占全球海运石油贸易的30%。

- 这是流量冲击,不是库存问题。石油市场依赖于持续的吞吐量,而不是静态存储。

- 如果中断持续超过几周,布伦特原油可能会从短期飙升转向更广泛的价格冲击,存在滞胀风险。

- 穿越海峡的油轮运输量从每天约135艘下降到中断高峰期的不到15艘船只,减少了约85%,超过150艘船只停泊、改道或延误。

- 4月8日宣布了为期两周的停火,为期45天的休战谈判正在进行之中。伊朗已分别表示要求对使用该海峡的船只收取过境费,如果正式确定,这将是能源成本的永久地缘政治最低标准。

- 市场已经开始从增长和技术敞口转向能源和国防企业,这反映了人们的观点,即石油价格上涨正在成为结构性成本,而不是暂时的风险溢价。

世界上最关键的石油阻塞点

霍尔木兹海峡每天处理大约2000万桶石油和石油产品,相当于全球石油消费量的20%和全球海运石油贸易的30%左右。由于全球石油需求接近1.04亿桶/日,且剩余产能有限,在最近的升级之前,市场已经处于紧密平衡状态。

该海峡也是液化天然气的重要走廊。2024年,平均每天约有2.9亿立方米的液化天然气通过该路线,约占全球液化天然气贸易的20%,亚洲市场是主要目的地。

国际能源署(IEA)将霍尔木兹描述为世界上最重要的石油运输阻塞点,并指出,即使是部分中断也可能引发价格的大幅波动。布伦特原油已跌破每桶100美元,这既反映了物质紧张,也反映了地缘政治风险溢价的上升。

由于流量减慢,油轮处于空转状态

现在,航运和保险数据实时显示压力。据报道,超过85艘大型原油运输船滞留在波斯湾,而由于运营商重新评估安全和保险,有150多艘船舶停泊、改道或延误。据估计,这将使1.2亿至1.5亿桶原油在海上闲置。

这些量仅代表霍尔木兹正常吞吐量的六到七天,或略高于一天的全球石油消费。

最新的航运和保险数据现在证实,有150多艘船只停泊、改道或延误,高于最初报告的85艘船只。闲置原油的1.3天全球消费保障仍然是约束性制约因素:这是流量冲击,不是储存问题,停火尚未转化为产量的实质性恢复。

建立在流量而不是存储基础上的市场

石油市场在持续波动中运作。炼油厂、石化厂和全球供应链经过调整,可以沿着可预测的海道稳定交付。当流经占全球石油消耗量约五分之一和全球海运石油贸易约30%的阻塞点时,该系统可以在几天之内从平衡变为赤字。

剩余产能主要集中在欧佩克内,估计仅为每天300万至500万桶。这远低于霍尔木兹水流受到严重干扰时面临的风险交易量。

Oil market analysis

How long do idle tankers last?

135M idle barrels — days of cover against each demand benchmark

vs. Strait of Hormuz daily flow (20M bbl/day)

vs. Global oil consumption (104M bbl/day)

vs. US Strategic Petroleum Reserve release (1M bbl/day)

135M

idle barrels on tankers (midpoint of 120–150M range)

~33%

of daily Hormuz flow that is idle storage, not transit

<31 hrs

is all idle storage against global daily consumption

通货膨胀风险和宏观溢出效应

石油冲击的通货膨胀影响通常以波浪形式出现。随着汽油、柴油和电力成本的上涨,燃料和能源价格的上涨可能会迅速提振总体通货膨胀。

随着时间的推移,更高的能源成本可能会流向货运、食品、制造业和服务业。如果混乱持续下去,通货膨胀率上升和增长放缓相结合,可能会增加滞胀环境的风险,使中央银行面临艰难的权衡。

不容易抵消,系统几乎没有松弛

当前局势之所以特别严重,是因为全球体系缺乏松弛。

当处理近2,000万桶/日(约占全球石油消耗量的五分之一)的阻塞点受到损害时,将近1.03亿至1.04亿桶的全球供需几乎没有备用缓冲。估计每天300万至500万桶的剩余产能,主要在欧佩克内部,只能覆盖风险产量的一小部分。

替代路线,包括绕过霍尔木兹的管道和改道运输,只能部分抵消流量的损失,而且通常成本更高,交货时间更长。

底线

在霍尔木兹海峡的过境恢复并被视为可靠安全之前,全球石油流动可能继续受损,风险溢价上升。对于投资者、政策制定者和企业决策者来说,核心问题是石油能否每天不间断地转移到需要去的地方。

Asia-Pacific markets head into this week focused on China’s growth data, potential JPY volatility with a Bank of Japan (BoJ) meeting week, and Australia's labour force report and commodity prices. Geopolitical events also remain in focus globally, and the US earnings season’s progression may indirectly influence sentiment.

Quick facts:

- China: Q4 GDP and December industrial production data will be read as a test of whether growth is stabilising or simply slowing more gradually.

- Japan: The BoJ meets 22–23 January, and Japan CPI (Dec) is due on 23 January, keeping USD/JPY and rates in focus.

- Australia: Labour Force (Dec) is the key local catalyst, alongside whether metal prices continue to support the materials sector.

China

What to watch:

China’s focus shifts to hard activity data, with Q4 GDP and December activity indicators offering a read on growth momentum into 2026. Markets are increasingly focused on whether recent policy support is translating into clearer traction in the real economy.

Key releases:

- Mon 19 Jan: Q4 GDP, December industrial production (primary). Retail sales and fixed asset investment (secondary).

How markets may respond:

- Growth-sensitive sectors in Chinese equities may react if the data reinforces that domestic demand remains soft, especially if headline GDP diverges from expectations.

- Australian assets may respond to GDP and industrial output outcomes, with implications for materials stocks. The data may also influence AUD sentiment following recent consolidation.

Japan

With the BoJ meeting later in the week, markets may see pre-decision volatility as positioning shifts around how hawkish the BoJ narrative may be. While consensus expectations often lean toward no change, the statement and press conference will be watched closely for any change in tone.

Key events:

- Fri 23 Jan: Bank of Japan rate decision and press conference (high sensitivity)

- Fri 23 Jan: Japan CPI (Dec) (medium sensitivity)

- Thu 22 Jan: Trade statistics — first 20 days of Dec (provisional) (low sensitivity)

How markets may respond:

- USD/JPY: Often acts as a fast channel for repricing Japan risk during BoJ weeks, particularly if guidance shifts expectations for the next move.

- Nikkei 225: Japanese equities can remain responsive to FX stability, particularly across exporter-heavy sectors. All-time high levels of 54000 will be watched as a key level.

Australia

Australia’s week is dominated by the employment data, with external influences from China’s data and broader global risk conditions also in view. Markets will likely focus on the balance between employment growth and participation and what it implies for Reserve Bank of Australia (RBA) expectations.

Key release:

- Thu 22 Jan: Labour force, Australia (Dec) (high sensitivity)

How markets may respond:

- ASX 200: Domestic cyclicals can react to the rates takeaway more than the headline jobs number. After the material-driven move back over 8800, this week will be key in determining whether a test of the psychologically important 9000 is on the cards.

- AUD/USD: Rate expectations can shift quickly. A stronger-than-expected jobs result could support the AUD, while a weaker print (or a rise in unemployment) could weigh on it.

Asia-Pacific calendar summary (AEDT)

- Mon 19 Jan: China GDP (Q4), industrial production and retail sales

- Tue 20 Jan: China Loan Prime Rate (1Y/5Y) (Jan)

- Thu 22 Jan: Australia employment (Dec); Japan trade statistics — first 20 days of Dec (provisional)

- Fri 23 Jan: BoJ rate decision and press conference; Japan CPI (Dec). PMI manufacturing in Australia and Japan.

Bottom line

Asia-Pacific markets enter the week with China’s growth data setting the regional tone, Japan facing heightened FX sensitivity into a BoJ meeting, and Australia focused on labour-market signals alongside commodity price direction.

Chinese GDP and industrial production are a test of whether activity is stabilising, with implications for regional risk appetite, materials pricing and the AUD.

In Japan, any shift in BoJ communication could drive USD/JPY volatility and spill into broader equity sentiment. For Australia, local employment data and external influences, particularly China and global risk conditions, are likely to shape short-term expectations across rates, equities and currency markets.

The Australian Securities Exchange (ASX) is one of the world's top 20 exchanges, hosting over 2,000 listed companies worth approximately $2 trillion.

Quick Facts:

- The ASX operates as Australia's primary stock exchange, combining market trading, clearinghouse operations, and trade and payment settlement.

- It represents roughly 80% of the Australian equity market value through its flagship ASX 200 index.

- 2,000+ companies and 300+ ETFs are listed on the exchange, spanning from mining giants to tech innovators.

How does the ASX work?

The ASX combines three critical functions in one system.

As a market operator, it provides the electronic platform where buyers and sellers meet. Trading occurs through a sophisticated computer system that matches orders in milliseconds, replacing the traditional floor-based trading that once defined stock exchanges globally.

The exchange also acts as a clearinghouse, ensuring trades settle correctly. When you buy shares, the ASX guarantees the transaction completes, managing the transfer of securities and funds between parties.

Finally, it serves as a payments facilitator, processing the money flows that accompany each trade. This integrated approach reduces settlement risk and keeps the market running smoothly.

What are ASX trading hours?

The ASX operates from 10:00am to 4:00pm Sydney time (AEST/AEDT) on business days, with a pre-open phase from 7:00am.

Stocks open alphabetically in staggered intervals starting at 10:00am, followed by continuous trading until the closing auction at 4:00pm.

The exchange observes Australian public holidays and adjusts for daylight saving time between October and April, which can affect coordination with international markets.

Top ASX Indices

S&P/ASX 200

This is the exchange's flagship index. It tracks the 200 largest companies by market capitalisation and represents approximately 80% of Australia's equity market.

It serves as the primary benchmark for most investors and fund managers and is rebalanced quarterly to ensure it reflects the current market leaders.

All Ordinaries Index

Commonly called the All Ords, this index covers the top 500 companies on the ASX.

It provides broader market exposure than the S&P/ASX 200, capturing roughly 80-90% of total market value.

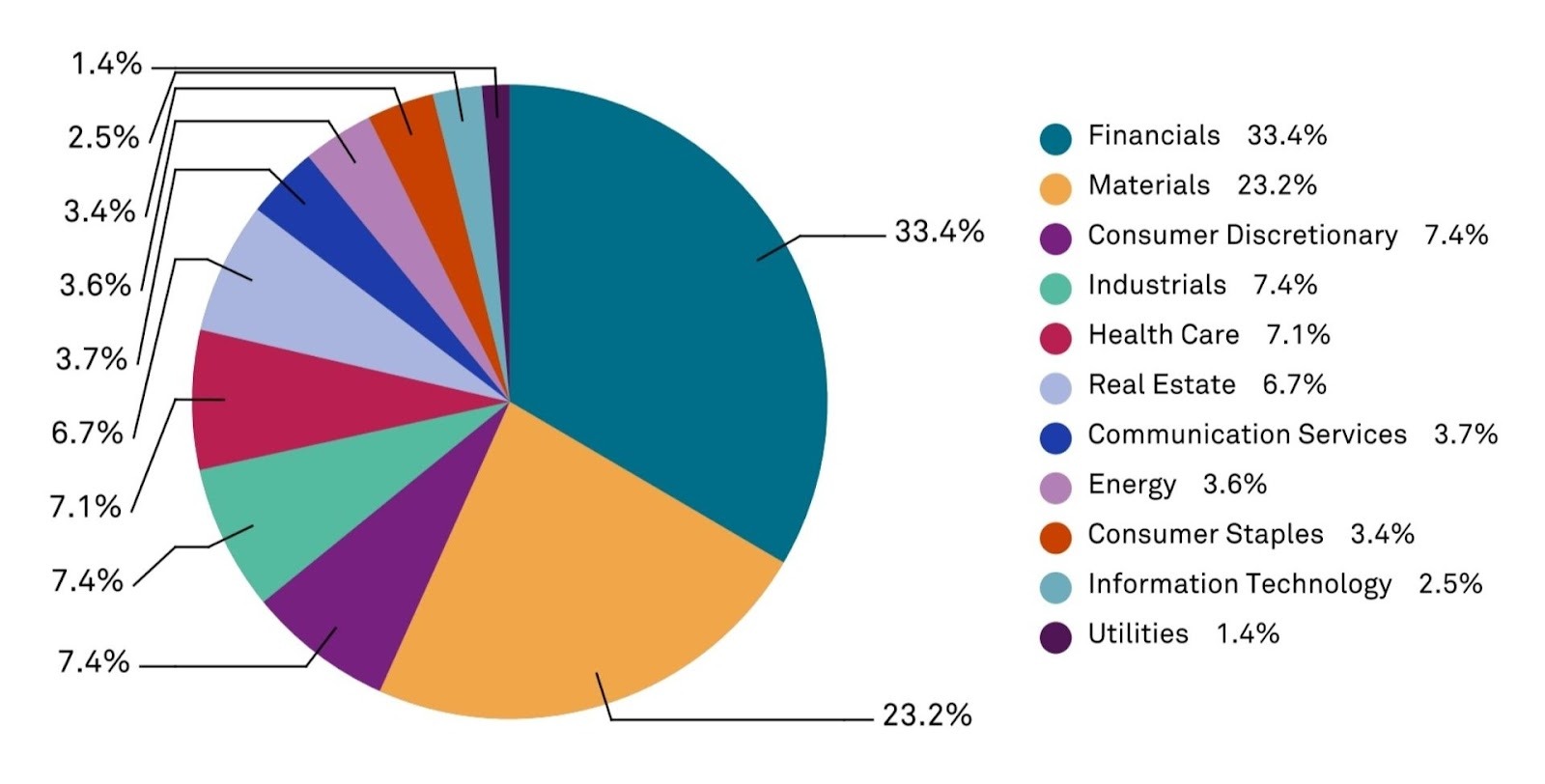

The 11 ASX sectors

The ASX also breaks down into 11 sector-specific indices, allowing investors to track performance in areas like financials, materials, healthcare, and technology.

These indices can help identify which parts of the Australian economy are strengthening or weakening.

- Financials dominates as the largest sector, driven by Commonwealth Bank, NAB, Westpac, and ANZ. These banking giants provide lending, wealth management, and insurance services across Australia.

- Materials ranks second, led by mining powerhouses BHP and Rio Tinto. This sector extracts and processes resources, including iron ore, coal, copper, and gold.

- Consumer Discretionary includes retailers, media companies, and hospitality groups that benefit when household spending rises.

- Industrials encompasses construction firms, airlines, and professional services businesses.

- Healthcare features companies like CSL, a global biotech leader, and Cochlear, which produces hearing implants.

- Real Estate features property developers and Real Estate Investment Trusts (REITs) that own and manage commercial and residential assets.

- Communication Services includes telecommunications providers like Telstra alongside media and entertainment companies.

- Energy tracks oil and gas producers (many renewable energy companies typically fall under utilities).

- Consumer Staples covers essential goods providers like supermarkets and food producers.

- Information Technology includes software developers and IT services firms.

- Utilities covers electricity, gas, and water suppliers, including renewable energy.

Top ASX companies

Three companies consistently lead the S&P/ASX 200 by market capitalisation.

Commonwealth Bank (Mkt cap: A$259 bln)

Commonwealth Bank holds the top position on the ASX as Australia's biggest lender.

Founded in 1911 and fully privatised by 1996, CBA offers retail banking, business lending, wealth management, and insurance.

Its performance often signals the health of the domestic economy.

BHP Group (Mkt cap: A$241 bln)

BHP Group stands as the world's largest mining company.

Its diversified portfolio spans iron ore, copper, coal, and nickel operations globally.

It serves as a bellwether for Australian commodity markets.

CSL Limited (Mkt cap: A$182 bln)

CSL Limited leads the Australian healthcare sector as a global biotech firm.

Established in 1916, CSL develops treatments for rare diseases and manufactures influenza vaccines.

The company demonstrates Australian innovation competing on the world stage.

The ASX's role in Australia's economy

The ASX serves as a vital mechanism for capital formation in Australia. It tends to provide price signals that reflect market expectations.

When share prices rise, it suggests optimism about economic conditions. Falling markets may indicate concerns about future growth.

Australian companies raise funds through initial public offerings and follow-on share sales on the ASX, using proceeds to expand operations, fund research, or pay down debt.

Investors in these shares benefit from potential capital gains and dividend income. Many Australians build retirement savings through superannuation funds that invest heavily in ASX-listed companies.

Employment in financial services also depends partly on a healthy stock market. Brokers, analysts, fund managers, and supporting roles exist because of active capital markets.

Key takeaways

The ASX functions as a market operator, clearinghouse, and payments facilitator, providing the infrastructure that enables capital formation and supports retirement savings for millions of Australians.

Its flagship index, the S&P/ASX 200, tracks the 200 largest companies and captures about 80% of market capitalisation, while the All Ordinaries index covers the top 500.

Financials and Materials dominate the exchange, led by Commonwealth Bank, BHP, and CSL, reflecting Australia's strength in banking and resources.

You can trade the S&P/ASX 200 Index CFD and over 230 ASX Share CFDs on GO Markets.

US earnings season is where the market gets its cleanest burst of new information. For Australians, it usually lands while the country is asleep. This is not just “US company news”. It is the scoreboard for the Nasdaq, the S&P 500, and risk appetite more broadly, with spillover into SPI futures, the AUD, and sector mood at the ASX open.

What this guide covers

- The four-wave rhythm (why volatility clusters in predictable months)

- The order of play (banks → tech → retailers) and what each group tends to reveal

- Before market open (BMO) vs after market close (AMC)

- The few lines markets care about (surprise vs expectations, and the forward reset)

- How earnings information can flow through to Australia via futures, FX, and sector sentiment

US earnings season basics

Earnings season is the 4 to 6-week window after each quarter when most US-listed companies report a new set of numbers and a new story.

Calendar rhythm and clustering

Earnings does not arrive as a smooth drip. It typically arrives in four recurring waves. Most US reporting clusters around January, April, July, and October. Each wave covers the prior quarter, which is why markets spend the lead-up period building expectations, then reprice quickly as numbers and guidance hit.

The sequence is familiar: banks open, tech dominates the middle, retailers close. That order matters because each group updates a different part of the macro story. If you only track one set of reports, make it the Magnificent 7 — here’s the Mag 7 earnings calendar for 2026 (Aussie-friendly timing)

.png)

Time zones: the two windows

For Australians, the key is when the first move hits.

- AMC (after market close): often Sydney and Melbourne morning, sometimes near the ASX open

- BMO (before market open): often late night, with the initial reaction while Australia sleeps

Daylight saving shifts timings, but the structure is consistent: two windows, two different liquidity conditions.

How the market digests an earnings event

Earnings is rarely a single reaction. It is a sequence.

- Headline release (EPS and revenue versus consensus)

- Immediate price discovery (often in after-hours or pre-market liquidity)

- Call and Q&A (guidance, margins, and demand tone get tested)

- Next US cash session (follow-through, reversals, broader positioning)

- Australia opens into the aftershock (futures, FX, and sector mood already set)

Translation: volatility often clusters around reporting windows because the calendar can concentrate new information and repricing.

Expectations: the scoreboard the market uses

Markets do not price “good” or “bad” in isolation. They price the gap versus expectations, then adjust the forward story. That is why the same quarter can look strong on paper and still disappoint if it lands below what the market had already baked in.

Most headlines boil down to three checks. First, actual results versus consensus. Second, actual results versus what the company previously guided. Third, quality and durability. That tends to show up in margins, the mix across segments, and whether cash flow backs up the earnings number.

Guidance: the forward reset

Guidance is where the narrative can change without the quarter changing. A company can deliver the past cleanly, then move the goalposts for what comes next. That forward reset is often what drives the bigger repricing.

In practice, guidance usually lands in a few buckets. Revenue or EPS outlook sets the top-line and earnings path. Margin outlook tells you how confident management is about costs and pricing. Capex language signals how heavy the investment cycle is likely to be. Capital return talk, including buybacks, is a read on balance sheet posture and priorities.

Translation: markets trade forward narratives. Guidance is the mechanism.

The call: where tone becomes data

Prepared remarks are polished. The call is where the market stress-tests the story. The Q&A is where the edges show up, because that is where analysts push on the parts that matter and management has to answer in real time.

Listen for the tells. Demand language can shift from broad to patchy. Pricing can move from power to pressure. Margin confidence can sound steady or start to carry caveats. And the “we are not breaking that out” moments matter too. What management avoids can be as informative as what it highlights.

Key takeaways

- Earnings season clusters in four waves (January, April, July, October), so volatility often arrives in blocks.

- The sequence matters. Banks open the read on confidence, tech steers index tone, retailers often close the consumer chapter.

- From Australia, BMO and AMC are the two windows that shape what you wake up to.

- Markets trade surprise vs expectations, then the forward reset via guidance and call tone.

- The spillover typically shows up through futures, FX, and sector sentiment before the ASX open.

Glossary (quick definitions)

- EPS: earnings per share

- Consensus: the market’s compiled estimate set

- Guidance: management’s forward-looking outlook ranges/comments

- Margins: profitability as a percentage of revenue

- Capex: capital expenditure (investment spend)

- BMO/AMC: before market open / after market close (US reporting labels)

- After-hours / pre-market: trading sessions outside regular US cash hours

- Correlation: how tightly assets move together (often rises in macro or de-risking periods)

As geopolitical narratives continue to simmer, US and European markets move into the rest of the week with three dominant drivers: US inflation data, the start of US earnings season, and an unusual Fed-independence headline risk after the DOJ subpoenaed the Federal Reserve.

Quick facts:

- US consumer price index (CPI) and producer price index (PPI) are the key macro releases and are likely to impact the US dollar (USD) and other asset classes if there is a significant move from expectations.

- JPMorgan reports Tuesday, with other major US banks through the week, as the Q4 reporting season gets underway.

- Reporting around DOJ action involving the Fed, and Chair Powell’s prior testimony, created early market volatility on Monday, with markets sensitive to anything that may be perceived as undermining Fed independence.

- President Trump announced this morning that any country doing business with Iran will face a 25% tariff on all business with the US, effective immediately.

- Europe’s production and growth updates, including Eurozone industrial production and UK monthly GDP and trade data, are later in the week.

United States: CPI, Fed path, DOJ and Fed headline risk, and banks leading earnings

What to watch:

The US is carrying the highest event density in global data releases this week. CPI and PPI will both be watched for moves away from expectations.

Any meaningful surprise can shift Fed policy expectations. Markets are currently pricing a lower likelihood of a March rate cut (under 30%) than this time last week, based on fed funds futures probabilities tracked by CME FedWatch.

Bank earnings may set the tone for the reporting season as a whole. Forward guidance is likely to be as important as Q4 performance, with valuations thought to be high after another record close in the S&P 500 overnight.

Key releases and events:

- Tue 13 Jan (Wed am AEDT): CPI (Dec) (high sensitivity)

- Tue 13 Jan (Wed am AEDT): JPMorgan earnings before market open (high sensitivity for banks and risk tone)

- Wed to Thu: additional large-bank earnings cluster (high sensitivity for financials sentiment)

- Wed 14 Jan (Thu am AEDT): US PPI

- Thu 15 Jan (Fri am AEDT): US weekly unemployment

- Throughout the week: Fed member speeches

How markets may respond:

S&P 500 and US risk tone: US indices are near record levels. The S&P 500 closed at 6,977.27 on Monday. Hotter-than-expected inflation can pressure growth and small-cap equities in particular, and weigh on the market broadly. Softer inflation can support further risk-on behaviour.

USD: Inflation data is the obvious driver this week for the greenback, but any continuation of DOJ and Fed developments, or geopolitical escalation, may introduce additional USD influences.

With the USD testing the highest levels seen in a month, followed by some light selling yesterday, some volatility looks likely. Gold has also been bid as a potential safety trade and hit fresh highs in the latest session, suggesting demand for defensive exposure remains present.

Earnings (banks): In a market already priced near highs, results can still create volatility if they are not accompanied by supportive earnings per share (EPS), revenue and forward guidance. Financials will likely see the first-order response, but any early pattern in results and guidance can influence the broader market beyond the first few days.

UK and Eurozone: growth data influence amid continuing equity strength

What to watch:

In a week where Europe may be driven primarily by events in the US and geopolitical narrative, the Eurozone industrial production print is still a noteworthy local release.

In the UK, monthly GDP and trade numbers on Thursday may influence both the FTSE 100 and the pound, particularly if there is any meaningful surprise.

Key releases and events:

Eurozone

- Wed 14 Jan: Eurozone industrial production (Nov 2025) (medium sensitivity for cyclical sectors)

UK

- Thu 15 Jan: GDP monthly estimate (Nov 2025) (high sensitivity for GBP and UK rate expectations)

- Thu 15 Jan: UK trade (Nov 2025) (low to medium sensitivity)

How markets may respond:

EUR spillover from the US: Despite light Eurozone data, the US response is likely to matter most this week, with the US dollar index a major driver of broader G10 FX direction.

DAX (DE40): Germany’s index is also trading at or near record levels and closed at 25,405 on Monday. (2) If the index is extended, it may react more to global rate moves and shifts in perceived risk.

FTSE 100 and GBP: The FTSE hit a new high in the overnight session, driven particularly by materials and mining stocks. (5) Any GDP surprise can re-price GBP and UK equities quickly in an environment where growth concerns persist.

US and Europe calendar summary (AEDT)

- Wed 14 Jan: US CPI, US bank earnings kick-off (notably JPMorgan)

- Wed 14 Jan: Eurozone industrial production (Nov 2025)

- Thu 15 Jan: UK monthly GDP (Nov 2025) and UK trade (Nov 2025), US bank earnings continue

- Fri 16 Jan: US weekly unemployment, US bank earnings continue

Bottom line

- If US CPI surprises higher, markets may lean toward higher-for-longer interest rate pricing, which can pressure equity multiples and lift rates volatility.

- If bank earnings are solid but guidance is cautious, equities can still see two-way swings given index levels near records and high valuations.

- If DOJ and Fed headlines escalate, they may override normal data reactions to some degree. That could increase demand for perceived safe havens such as gold and lift FX volatility.

- For Europe, Eurozone production (Wed) and UK GDP and trade (Thu) are the key local data. The region is still likely to trade primarily off US outcomes and broader risk sentiment.

So why do Magnificent 7 (Mag 7) earnings matter for Australians? Because the US earnings season is a different sport from Australia, and this is where the scoreboard sits. These seven names do not just report results, they set the tone for the Nasdaq, the S&P 500, and risk appetite more broadly. They often influence index tone, but market moves are not guaranteed and can fade or reverse.

The Aussie edge: time zones, event windows, and what gets priced

For Aussie traders, the challenge is not just timing. It's overnight gaps, liquidity, and AUD/USD currency moves that can amplify or offset the share price reaction.

Most Mag 7 results land after the US close, so the initial move often hits Sydney morning liquidity. Markets may react first to the headline numbers, then again during the call as guidance, margins and capex are digested — but the sequence varies by quarter.

What this guide gives you, company by company

For each company, we map the US Eastern Time (ET) reporting window and the Sydney time window (AEDT), flag whether it is before or after the US close, and narrow the focus to the few drivers that tend to move price.

Apple Inc (NASDAQ: AAPL)

Apple is a “quality” print until it isn’t. The market doesn’t just ask if Apple beat. It asks whether demand and mix support the next leg.

Reporting window (confirmed)

- US reporting time: Thu, 29 Jan 2026 at 5:00 pm ET (after close)

- AU reporting time: Fri, 30 Jan 2026 at 9:00 am AEDT

Quarter snapshot (Q1)

- Projected consensus earnings per share (EPS): US$2.65

- Projected consensus revenue: US$135.86 billion (bn)

- Call focus: iPhone demand and mix, services trajectory, China and FX translation

Translation: Apple “beats” are common. The repricing comes from demand tone and margin language.

Earnings expectations and how the market will frame it

A “beat” means EPS and revenue come in above expectations, but it only really counts if demand still sounds healthy and the gross margin commentary stays straightforward.

A “meet” means results are basically in line, so attention shifts to the call. Investors will focus on iPhone product mix, how fast Services is growing, and whether any specific regions are weakening.

A “miss” often reacts more negatively if it is driven by weaker demand, because the market may treat it as the start of a trend, not a one time issue. You can also see a big price gap right after the report, before the call even starts.

Meta Platforms Inc (NASDAQ: META)

Meta is expected to report the December quarter, which effectively turns this into a Sydney morning catalyst for Aussie traders. The headline move hits first but the second leg often comes from the call, when guidance and capex ranges get priced.

Reporting window (expected)

- US reporting time: Mon, 2 Feb 2026 at 4:05 pm ET (after close)

- AU reporting time: Tue, 3 Feb 2026 at 8:05 am AEDT

Quarter snapshot (Q4)

- Projected consensus EPS: US$8.29

- Projected consensus revenue: US$58.27 bn

- Call focus: AI infrastructure capex, Ads demand plus Reels monetisation and Reality Labs losses versus discipline

Translation: Meta can beat the print and still sell off if the Street hears “higher spend, longer payoff.”

Earnings expectations and how the market will frame it

A “beat” means EPS and revenue come in above consensus, but it only really counts if guidance stays intact and the 2026 capex and expense ranges do not get wider.

A “meet” is close enough that the stock trades the tone of the call: how broad ad demand looks, whether Reels monetisation is improving, and whether spending sounds capped or more open ended.

A “miss” can turn ugly quickly if it comes with weaker ad demand commentary or higher spend bands. With expectations already high, the initial gap can be sharp, and what happens next depends on whether guidance can steady the story.

Alphabet Inc (NASDAQ: GOOGL)

Alphabet is still an ads engine first, and a Cloud and AI story second. The market wants proof that Cloud profitability and AI spend can coexist without compressing the whole narrative.

Reporting window (confirmed)

- US reporting time: Wed, 4 Feb 2026 at 4:00 pm ET (after close)

- AU reporting time: Thu, 5 Feb 2026 at 8:00 am AEDT

Quarter snapshot (Q4)

- Projected consensus EPS: US$2.59

- Projected consensus revenue: TBC

- Call focus: Search and YouTube ads pricing and volume, Cloud growth and profitability, AI capex and monetisation signals

Translation: The market forgives a lot if ads are strong and Cloud margins keep improving.

Earnings expectations and how the market will frame it

A “beat” means EPS and revenue come in above consensus, but it only really matters if ad demand sounds broad and Cloud profitability does not slip while AI spending ramps.

A “meet” puts the call in the driver’s seat, with investors listening for ad pricing trends, YouTube momentum, and whether capex is moving higher.

A “miss” hurts most if it is driven by weaker ads, because then the market starts debating the ad cycle, not just the company.

Amazon.com Inc (NASDAQ: AMZN)

Amazon is two businesses stapled together in the tape. The market uses AWS to price growth and uses retail margins to price discipline.

Reporting window (expected)

- US reporting time: Mon, 2 Feb 2026 at 4:00 pm ET (after close)

- AU reporting time: Tue, 3 Feb 2026 at 8:00 am AEDT

Quarter snapshot (Q4)

- Prijected consensus EPS: US$1.97

- Projected consensus revenue: US$211.33 bn

- Call focus: AWS growth and margins, retail profitability/fulfilment efficiency, advertising momentum, capex tone

Translation: AWS decides the direction. Retail decides the confidence.

Earnings expectations and how the market will frame it

A “beat” means EPS and revenue come in above consensus, but it only really matters if AWS holds steady or speeds up again and management does not worry the Street with spending plans.

A “meet” puts AWS and margin tone front and centre, and the call does most of the work.

A “miss” usually gets hit hardest when AWS growth slows or operating income guidance disappoints, because that is what can reset the whole valuation debate.

Microsoft Corp (NASDAQ: MSFT)

Reporting window (confirmed)

- US reporting time: Wed, 28 Jan 2026 at 4:00 pm ET (after close)

- AU reporting time: Thu, 29 Jan 2026 at 8:00 am AEDT

Quarter snapshot (Q2)

- Projected consensus earnings per share (EPS): US$3.86

- Projected consensus revenue: US$80.09 bn

- Call focus: Azure growth, AI monetisation (Copilot/attach), capex intensity, and margin trajectory

Translation: This is usually a cloud plus capex trade, not an EPS trade.

Earnings expectations and how the market will frame it

A “beat” means EPS and revenue come in above consensus, but it only really matters if Azure is holding up and capex does not sound unlimited. Beat plus steady cloud trends and stable margins is the upside script the tape usually rewards.

A “meet” puts the focus on the call, especially Azure growth, commercial bookings tone, and how quickly capex is stepping up.

A “miss” usually gets punished most when cloud growth slows or margins get shaky, because that is the key forward anchor the market leans on.

NVIDIA Corp (NASDAQ: NVDA)

Nvidia is the season’s last boss. Markets treat it like a read-through on AI capex itself. The print matters, but guidance and gross margin are the real price setters.

Reporting window (confirmed)

- US reporting time: Wed, 25 Feb 2026 at 4:20 pm ET (after close)

- AU reporting time: Thu, 26 Feb 2026 at 8:20 am AEDT

Quarter snapshot (Q4)

- Projected consensus EPS: US$1.45

- Projected consensus revenue: US$65.47 bn

- Call focus: Data centre demand versus capacity, gross margin trajectory, supply/lead times, next-quarter guide

Translation: Guidance and gross margin commentary often drive the reaction, but outcomes vary.

Earnings expectations and how the market will frame it

A “beat” means EPS and revenue come in above consensus, but it only really matters if the next quarter outlook confirms demand is still strong and the gross margin message stays solid.

A “meet” means the call becomes the decider, and the stock trades the outlook, margins, and what management says about supply conditions.

A “miss” can gap down fast, especially if it comes with softer forward guidance, because the market may take it as a clue about the broader AI spending cycle.

Tesla Inc (NASDAQ: TSLA)

Tesla’s earnings are rarely just about the quarter. The print hits first, but the real repricing usually happens when the call clarifies margins, demand, and the autonomy timeline. For Aussie traders, it’s a Sydney morning catalyst.

Reporting window (confirmed)

- US reporting time: Wed, 28 Jan 2026 at 4:05 pm ET (after close)

- AU reporting time: Thu, 29 Jan 2026 at 8:05 am AEDT

Quarter snapshot (Q4)

- Projected consensus EPS: US$0.44

- Projected consensus revenue: US$25.15 bn

- Call focus: Autonomy/robotaxi cadence, auto gross margin, pricing/demand and energy storage scale

Translation: Tesla can “beat” and still get sold if margins compress or the roadmap tone shifts.

Earnings expectations and how the market will frame it

A “beat” means EPS and revenue come in above consensus, but it only really matters if the margin story stays intact and management does not add fresh uncertainty around pricing or timing.

A “meet” is close enough that the stock trades the tone of the call, especially on demand, how durable margins look, and progress toward autonomy milestones.

A “miss” gets hit fastest when it comes with weaker margin language or softer demand comments, because the market will assume next quarter looks tougher, not easier.

Ahead of the US nonfarm payrolls (NFP) release (Friday, 9 January, 8:30 am ET/ Saturday, 10 January, 12:30 am AEDT), major US equity indices have been trading near recent highs (as at 9 January 2026).

Next week, attention is likely to shift to inflation data, any change in expectations for Federal Reserve (Fed) policy, and the start of US earnings season. Together, these may support or challenge current valuations.

Quick facts:

US inflation: The consumer price index (CPI) and producer price index (PPI) releases will test whether inflation is showing signs of persistence.

Earnings season: Major US banks report first, providing an early read on financial conditions and whether current valuations can hold up.

Gold futures: Gold futures remain close to record levels, with US dollar (USD) moves after key data a potential swing factor.

Geopolitics: Ongoing tensions remain on the radar and could influence risk sentiment.

US inflation data: could CPI and PPI shift rate-cut expectations?

Timing:

- CPI: Wednesday 14 January, 12:30 am AEDT

- PPI: Thursday 15 January, 12:30 am AEDT

CPI and PPI are the major scheduled macro events for the week. The updated inflation prints across consumer and producer prices will help markets assess whether disinflation is continuing or whether inflation is showing signs of persistence.

Market impact:

- A softer outcome could support risk sentiment and weigh on Treasury yields and the USD. However, reactions can vary depending on positioning and broader macro headlines, including how confidently markets price a March Fed rate cut.

- A stronger-than-expected reading may pressure equities and reinforce caution in bond markets.

US earnings season begins with the banks

Timing:

- JPMorgan Chase (JPM): Tuesday, 6:35 am ET

US earnings season begins with results from major banks, providing an early snapshot of financial conditions and economic momentum. Investor attention is likely to extend beyond headline earnings to guidance and management commentary.

Market impact

- Strong results versus earnings per share (EPS) and revenue expectations could support sentiment, particularly within financials.

- Cautious forward guidance may pressure share prices and could weigh on broader indices if it becomes a common theme.

- Early bank prints can shape expectations for the wider season. Watch how the first reporters in each sector influence related stocks.

Gold futures to retest record highs?

After a recent pullback, gold futures are trading within striking distance of record highs again. The backdrop remains a mix of geopolitical uncertainty and the potential for data-driven moves in the USD.

Market impact

- Continued strength could support a retest of late December highs around US$4,585.

- The short-term US$4,500 area may act as a short-term technical resistance in determining whether upside momentum can hold.

- Another pullback may occur if yields rise or the USD strengthens following key data releases.

Geopolitics remains in focus

Geopolitics remains a background market consideration, with headlines and broader policy messaging sometimes influencing risk sentiment. Markets have shown resilience to date, but sensitivity may rise if developments escalate.

Market impact

- Escalation could influence energy prices, defence stocks, and hedging assets such as gold.

- A cooling in the narrative may reduce volatility and allow markets to refocus on macro data and earnings.

Economic calendar

All dates and times may be subject to change.